Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

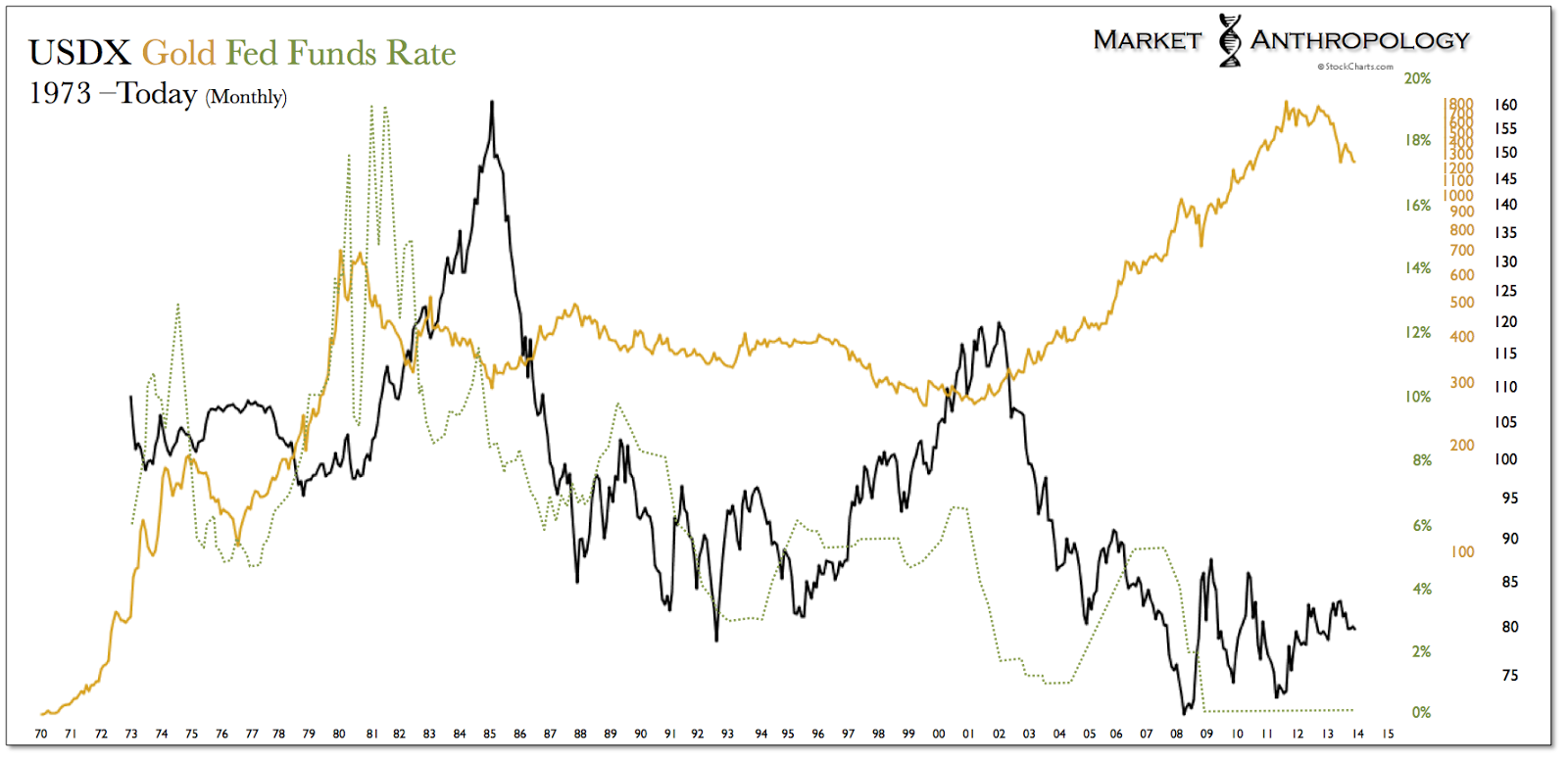

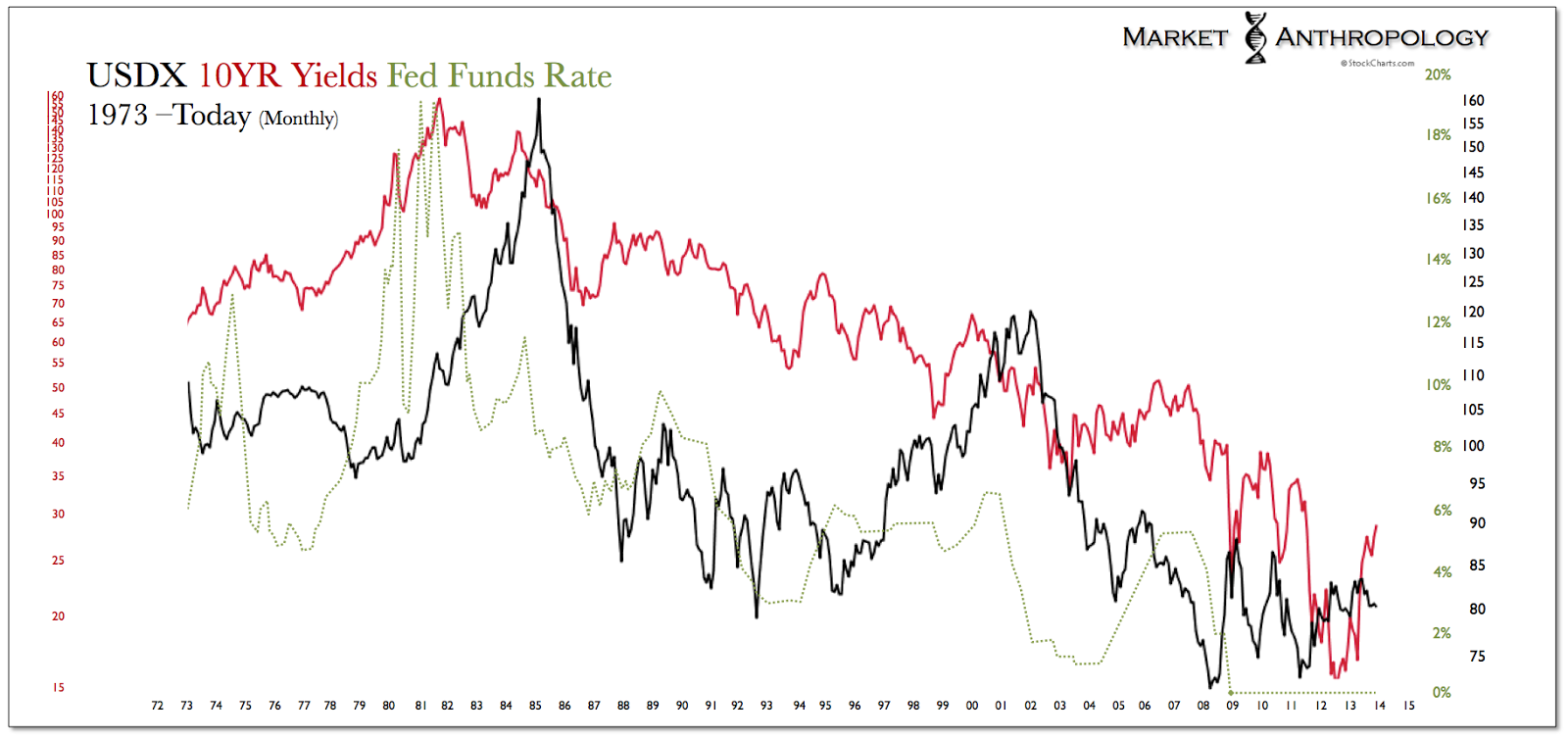

Despite what the academics and semantics present, we remain firmly in the tapering is tightening camp. Furthermore, while it’s not an apples-to-apples structural comparison (because of ZIRP and QE) to previous Fed cycles, we would argue that the esoteric nature of our current monetary policies introduces a greater behavioral catalyst for the markets to react, interpret and digest; thus, a longer lag-time between what the Fed implies and eventually does. Are they still exceptionally accommodative? You bet, but they’ve been trying to prepare the markets throughout the year that we are approaching a major pivot. In terms of where the rubber meets the road in the market, the bond boys voted unanimously this spring that even a mention and discussion by the Fed of the taper was equivalent to tightening these days.

The one constant you can depend on is that participants will overreact when the US dollar weakens. Point being, they egregiously misread the tea-leaves to indicate hyperinflation on the horizon with the two most recent occasions (08′ & 11′) when the dollar tested the lower limits of the range. With the quantitative reservoir now almost full and reaching the Fed’s flood gates – we expect to hear a very loud and boisterous third choir should the dollar double back around.