Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

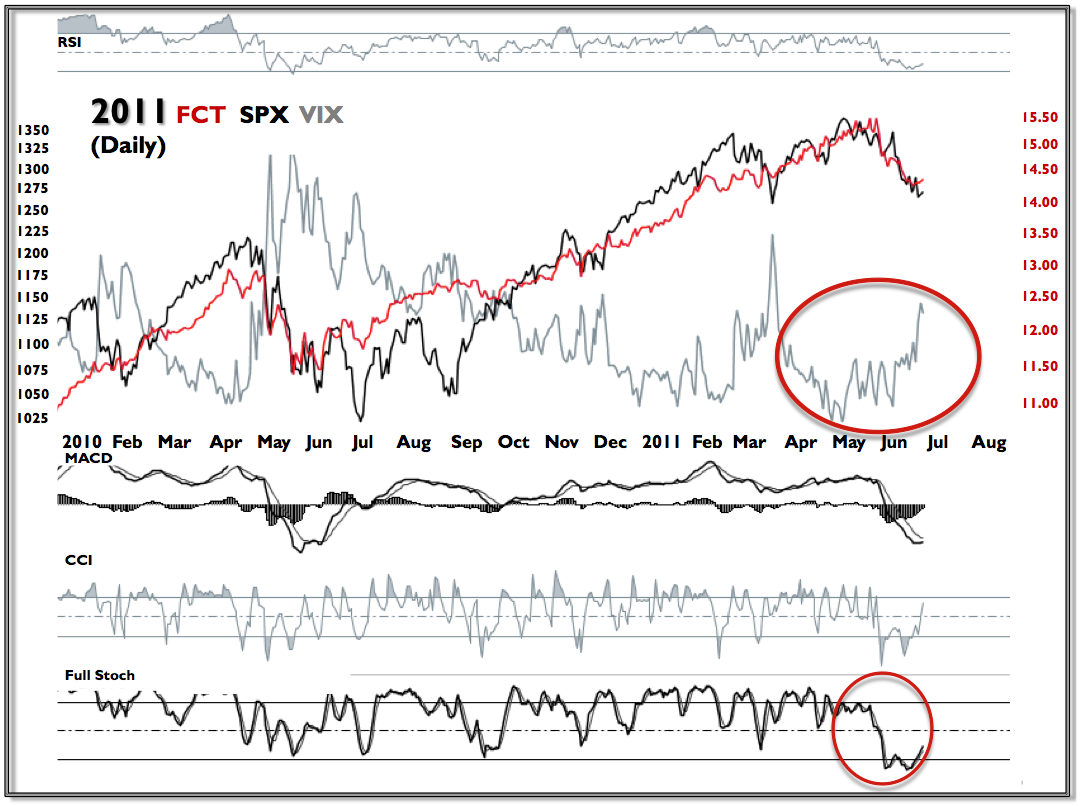

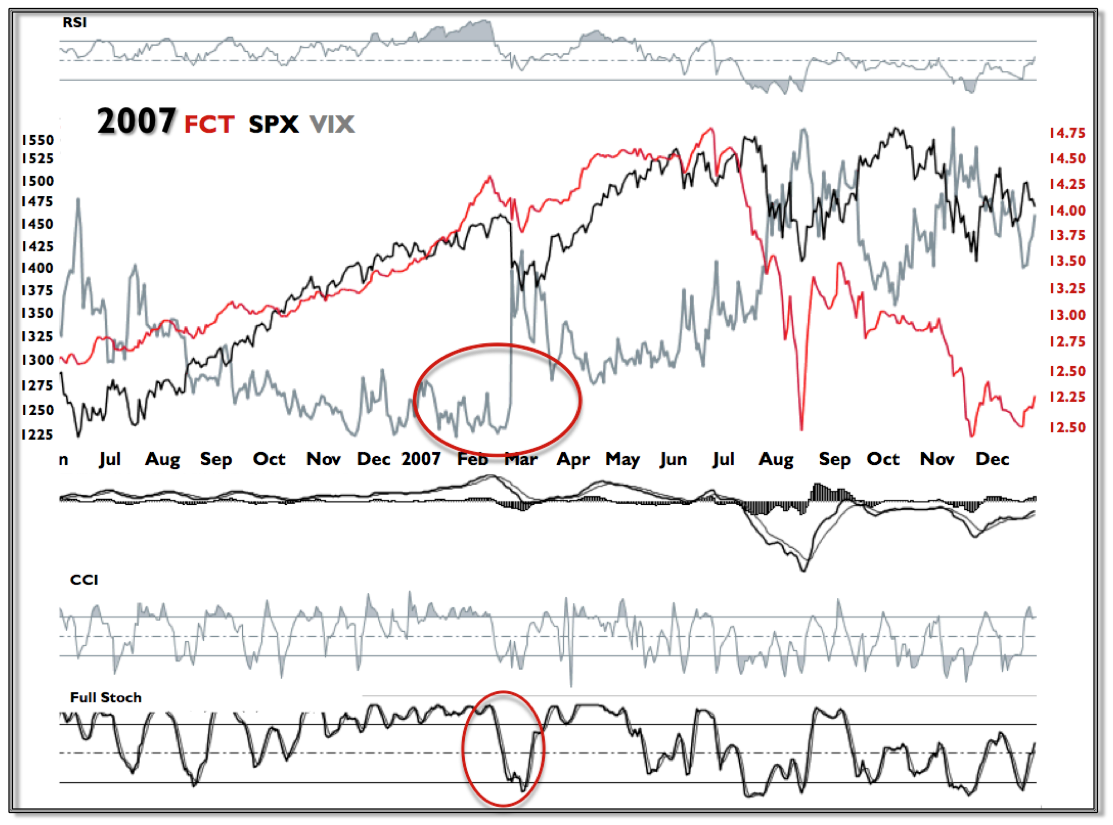

“One such tool has been to keep an eye on a position like FCT. FCT is a close ended fixed income mutual fund that primarily invests in senior floating rate loans made to mid tier corporate borrowers. Its utility on my screen has been to appraise credit risk sensitivity.”