Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

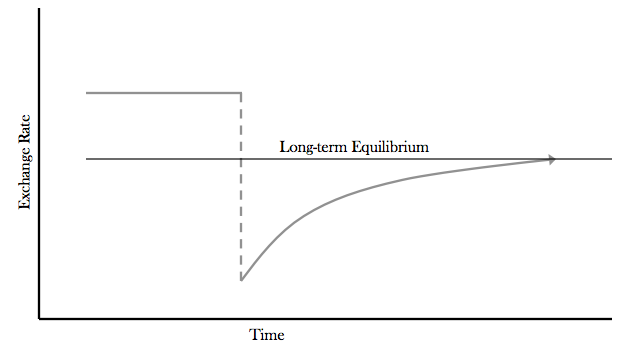

“According to the model, when a change in monetary policy occurs (e.g., an unanticipated permanent increase in the money supply), the market will adjust to a new equilibrium between prices and quantities. Initially, because of the “stickiness” of prices of goods, the new short run equilibrium level will first be achieved through shifts in financial market prices. Then, gradually, as prices of goods “unstick” and shift to the new equilibrium, the foreign exchange market continuously reprices, approaching its new long-term equilibrium level. Only after this process has run its course will a new long-run equilibrium be attained in the domestic money market, the currency exchange market, and the goods market.

As a result, the foreign exchange market will initially overreact to a monetary change, achieving a new short run equilibrium. Over time, goods prices will eventually respond, allowing the foreign exchange market to dissipate its overreaction, and the economy to reach the new long run equilibrium in all markets.“ – Exchange Rate Overshooting Hypothesis – Wikipedia

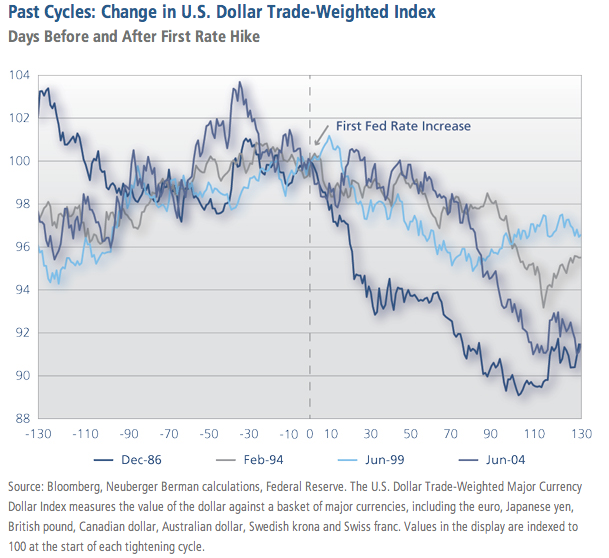

What happens to the dollar when the Fed actually begins to tighten? If past is prologue – and which we expect will ultimately be a significantly less aggressive tightening/normalizing cycle (but obviously still enacted relative to the extremely low inflation rates within Europe); the dollar should depreciate as a long-term equilibrium is re-established which reflects the inflation premium present in the U.S.. As shown in the Figure from Neuberger Berman, the dollar has strengthened in the previous four cycles during the expectation phase of tightening and typically begins to weaken even before the first rate hike is made by the Fed. For traders, this dynamic is commonly described as buy the rumor – sell the news; however, these days with the expectations of tightening beginning to modulate with U.S. economic growth, we think the reality may become: buy the hype – sell the bluff.

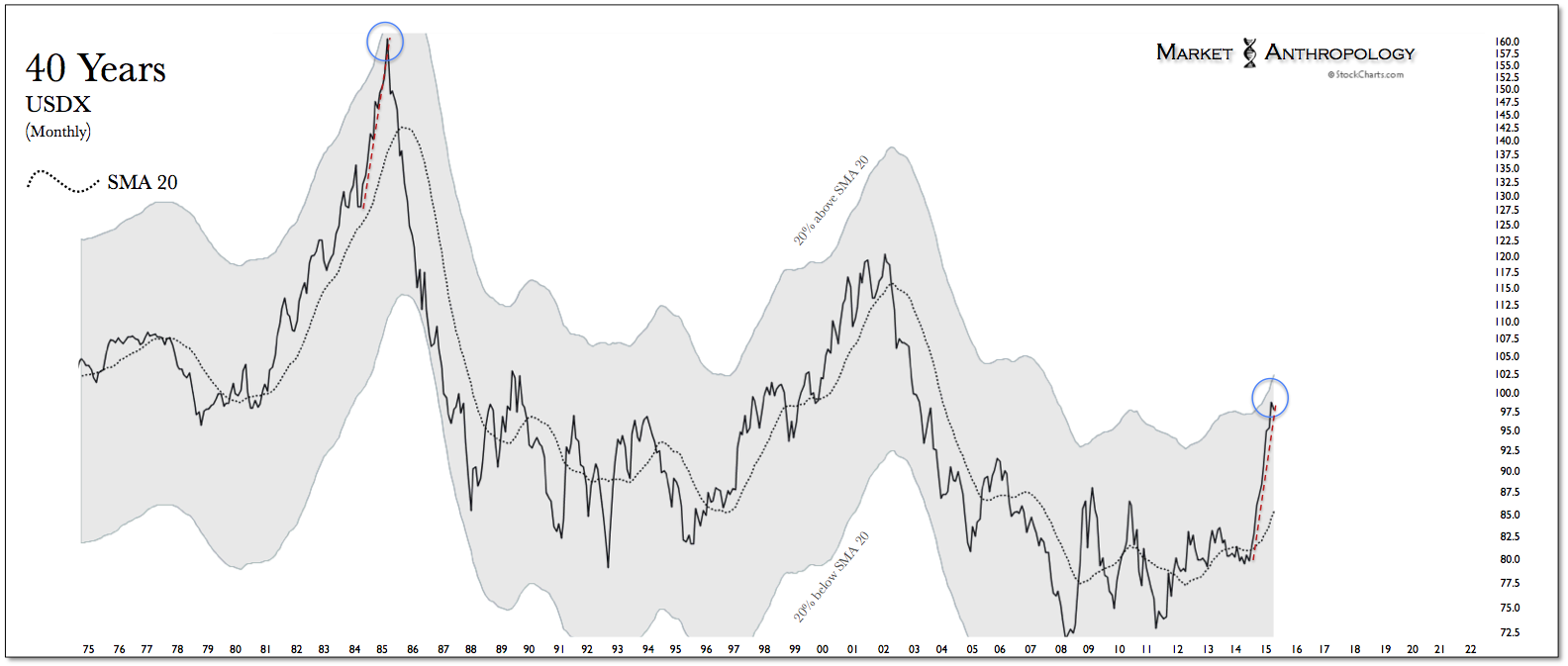

All things considered – and as we described in recent notes, the concentrated flows and behavioral biases taken up over the past year in the respective trends of the euro and dollar, has pushed the U.S. dollar index to a relative performance extreme, arguably last witnessed at the secular peak in the index in February 1985. In our opinion, despite the retracement rally in the U.S. dollar index this week, the extreme overshot in the euro dollar exchange rate may now be in the markets rearview mirror, which should go a long way in engendering a rising tide in inflation expectations, as the markets work their way back to a longer-term equilibrium.

From our perspective, assets positively impacted by rising inflation expectations, such as – precious metals and oil, should outperform, with retracement declines susceptible in the government bond markets. With German 10-year bunds yielding less than 0.2 percent – while Germany’s core CPI is expected to come in ~ 1.1% this year, it seems safe to speculate that the move in bunds has also lived up to expectations of Dornbusch’s overshooting model. The same could be said with oil, although you would be hard pressed to read as much in the financial media – which has continued to gravitate towards the fundamental supply side of that story, rather than the inherent denominating calculus in the currency markets that appears far more consequential to the price of oil today.

In either example, both German bunds and oil have witnessed market extremes (scarcity and oversupply) affected by the same overshooting dynamic, that we suspect will be normalized over the course of this year – as both assets work their way back to a longer-term equilibrium.

“If the ECB needs to execute the full “We don’t have much room left, but

program, it is going to be challenging we’re still answering the phones,”

if it stays like this,” said Elie El Hayek, says Mike Moeller, who manages

global head of rates and credit trading the company’s Cushing tank farm.

at HSBC. “There are not enough long- “Not everybody who calls is going

term bonds unless there is a short-term to get space.” Oil Storage Squeeze

selloff.” ECB Bond-Buying Program May Lead to Another Price Crash

Could Hinge on German Debt Supply – Bloomberg 3/12/15

– WSJ 3/30/15

Just how extreme was the move in yields in Europe? What took Japan over six years to travel, Germany exceeded in 16 months. A markets fundamentals were significantly overruled and overshot by profound shifts in monetary policy. Despite the conventional market wisdom now built around these relatively short-term moves, like Dornbusch’s model would suggest, we expect these assets to rebound/retrace back to their new long-term equilibriums; which in the case of the euro dollar exchange rate, oil and German 10-year yields – is likely substantially higher than current market conditions reflect.