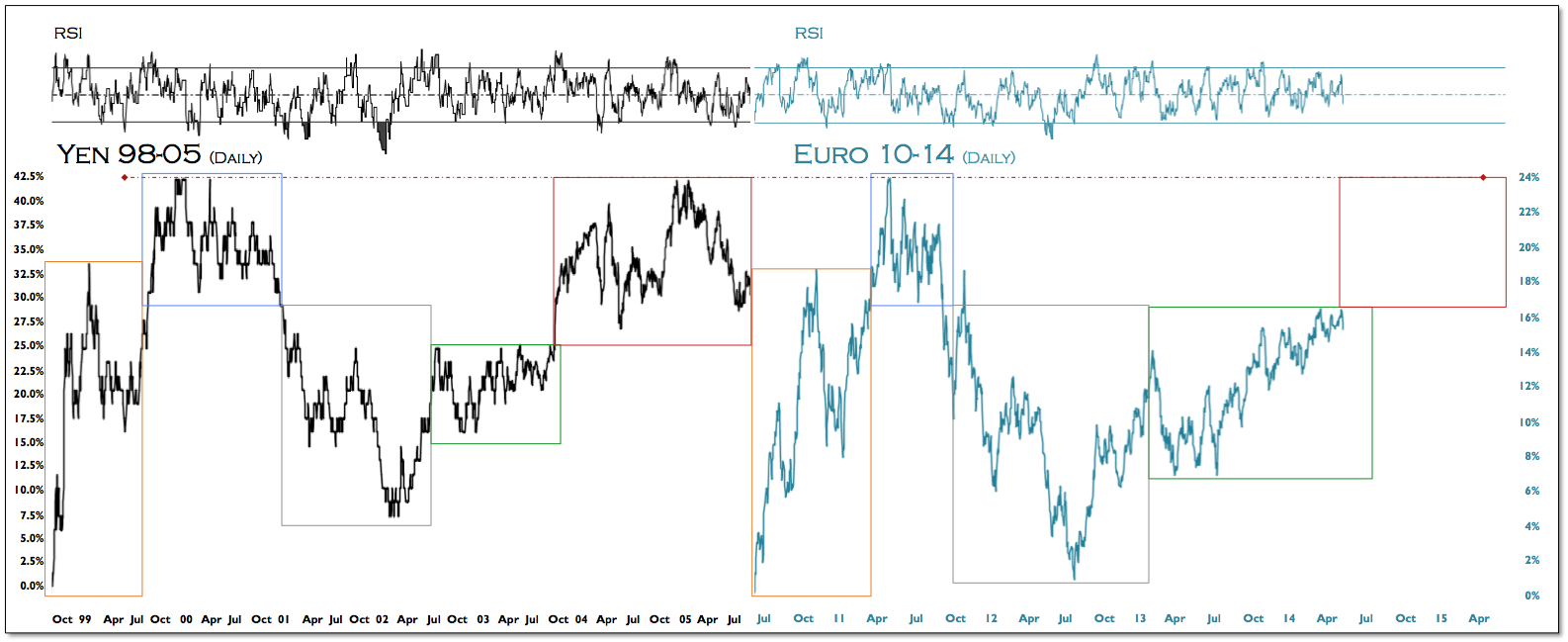

He huffed and he puffed and he blew the euro down. Puff the Magic Draghi delivered another breath of fire from the ECB’s bully pulpit yesterday, raising the stakes with more word play that the ECB would be “comfortable taking action in June”. While there seems to be a growing consensus of “this is it – they’re going to do it”, we would urge caution and consider the trend – as well as the structural transmission ambiguities that more unconventional monetary policies could impart on the euro. Less we forget, the historic record is not that impressive, when one considers the cause and effects between QE and the native currency, or the fact that the euro continues to climb one of the largest walls-of-worry ever constructed. Although we understand Draghi’s contractual agreements with jawboning the currency lower when he can, the truth is its effects are short-lived and the eventual breakout – should it come, more severe as the short-base grows increasingly entrenched. From a comparative point-of-view with the historic deflationary trend of the yen – circa 98-05, Draghi’s trying to prevent the red box outcome from materializing by staunchly defending 1.40 for now. Of dungeons and dragons, “Whatever it Takes” has come with existential consequences in an asymmetric monetary union.