Despite the strong GDP print yesterday that reinvigorated the raise-rates camp and sparked an almost 4 percent rally in 10-year yields, we continue to feel these participants are once again placing the cart before the horse, when it comes to what Chairwoman Yellen has repeatedly articulated will be a “considerable time” after the QE programs are wound down this October – and when they consider their next policy response.

From our perspective, where the rubber meets the road with the specifics of actually raising rates is much further off in the future and only after the markets normalize to this rather significant shift in support – from both a structural and psychological point-of-view. (For more of our thoughts on the effects of this normalization and why we don’t find parallels with recent history, see Here)

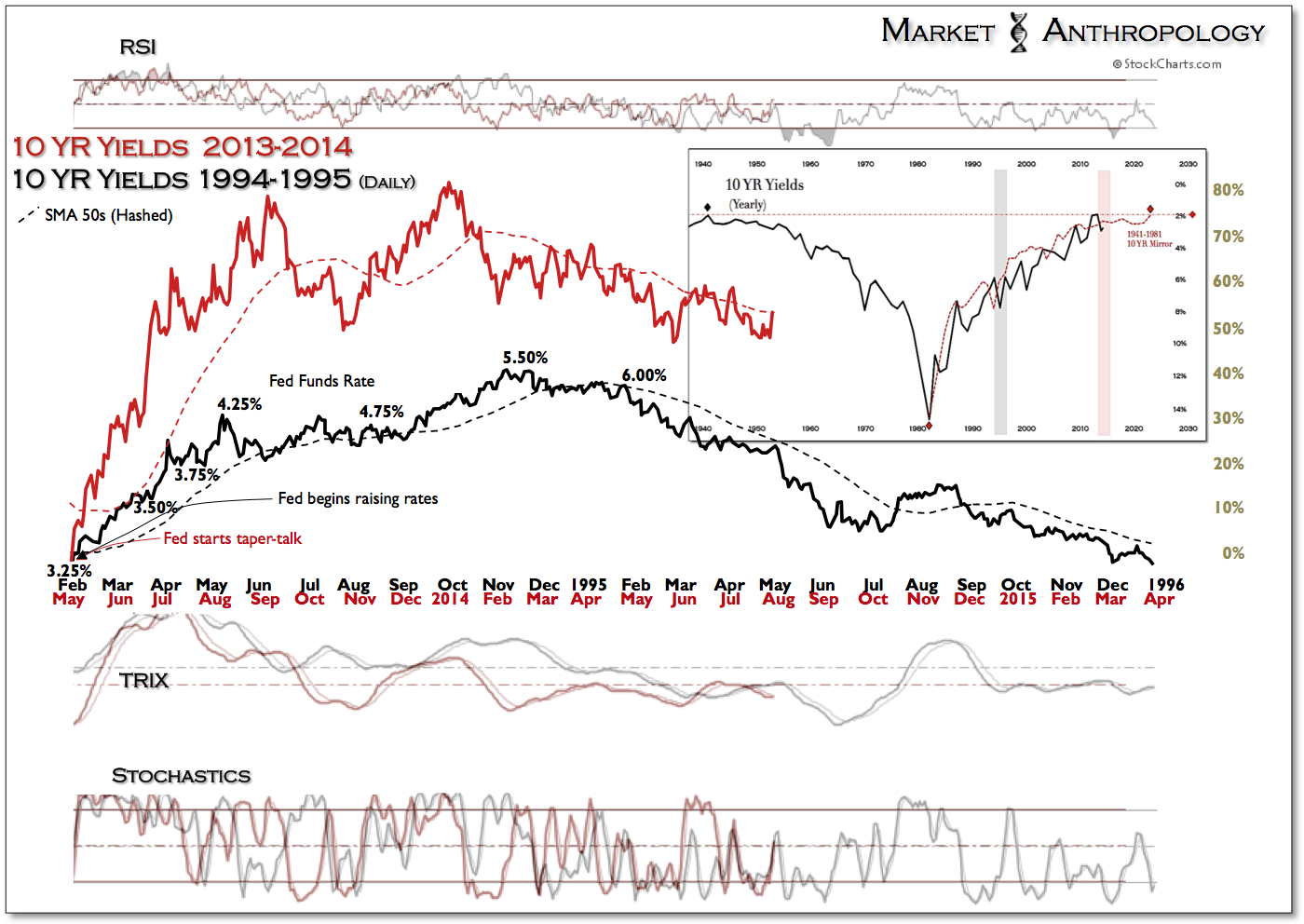

With respect to 10-year yields, the frictions from the end of QE should continue to support the Treasury market and we expect the next step lower in yields to be taken as the markets stroll into August.