Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

|

|

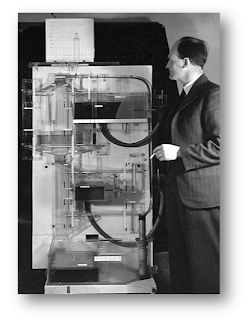

William Phillips

|

He saw that money stocks could be represented as tanks of water, and monetary flows by water circulating round plastic tubes.

With a grant of £100 (obtained with Newlyn’s help) he spent the summer of 1949 in a garage in Croydon ‘living on air’ as James Meade was later to put it, working on a hydraulic representation of the Keynesian model.

In the machine he constructed, the circular flow of income was represented by water being pumped round a series of clear plastic tubes, with outflows representing savings, taxes and imports, and inflows representing investment, government spending and exports. The model had three tanks representing the stock of money, one for transaction balances and one for foreign-held sterling balances. The whole system determined the level of income, the rate of interest, imports, exports and the exchange to an accuracy (astonishing at the time) of +two per cent. The time path of income and the other variables was traced out by plotter pens making it possible to analyse the quantitative effects of economic policy.

The machine, in the jargon, was a hydraulic representation of an open economy IS-LM model with an explicit underlying dynamic structure. It was this very Heath Robinson prototype which, with the enthusiastic support of James Meade (then Professor of Commerce at the School), Phillips demonstrated to Lionel Robbins’ seminar in November 1949. Those attending gazed in wonder at this large (7ft high x 5ft wide x 3ft deep) ‘thing’ in the middle of the room. Phillips, chain smoking, paced back and forth explaining it in a heavy New Zealand drawl, in the process giving one of the best lectures on Keynes that anyone in the audience had ever heard. Then he switched the machine on. And it worked! According to Lord Robbins’ recollections, “there was income dividing itself into consumption and saving…Keynes and Robertson need never have quarrelled if they had had the Phillips Machine before them” The Phillips Machine Project

Disclaimer: This is not investment advice. Always do your own due diligence. Erik Swarts is not a registered investment advisor. Under no circumstances should any content from this website be used or interpreted as a recommendation for any investment or trading approach to the markets. Trading and investing can be hazardous to your wealth. Any investment decisions must in all cases be made by the reader or by his or her registered investment advisor.