Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

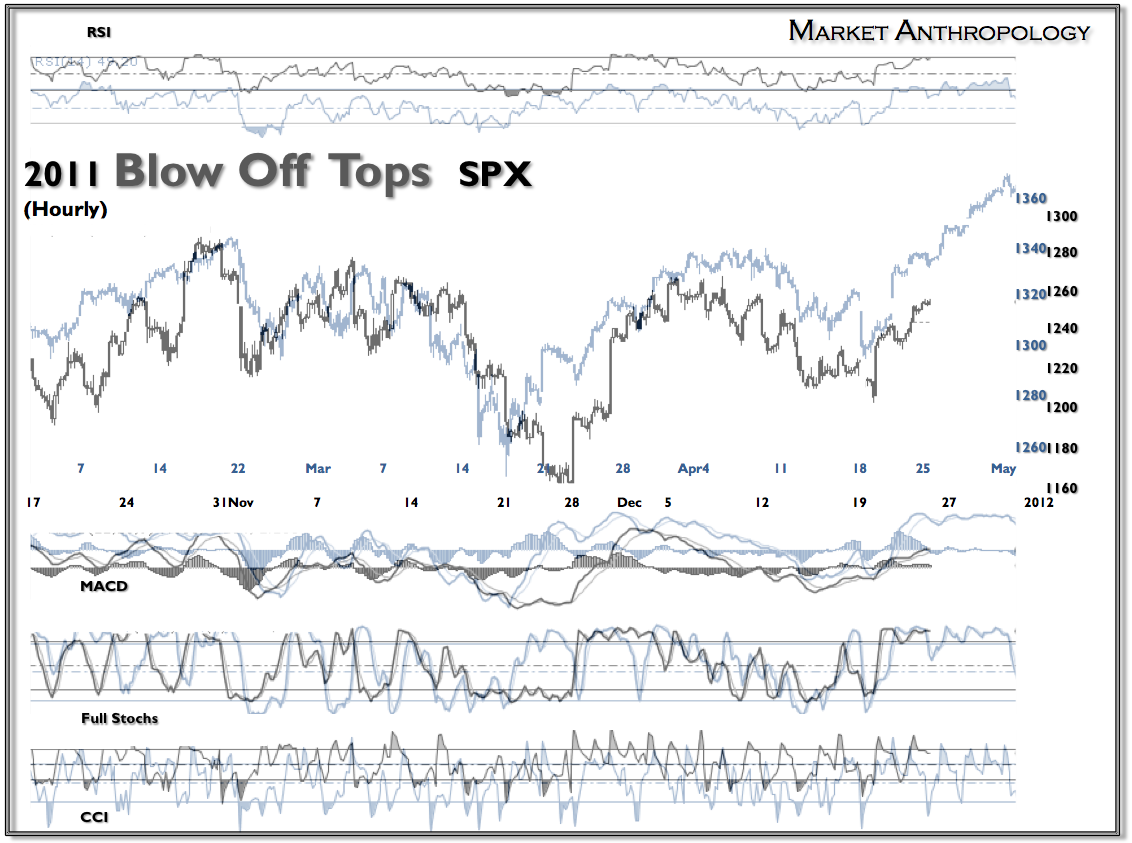

“The respective momentum metrics colored my expectations for a slightly weaker market, hence a deeper pivot than the comparative analog. This difference is one of the primary reasons why I believe the market will have a lower proportional high than the comparative period in May. In May, the market exceeded the March high by approximately 2%. That comparison would roughly work out to a target high for this move to ~ 1318. I believe that will not be reached, with 1300 serving as the top of the range for this move.” – “Blowing Off”