In the wake of another Fed decision, frustrations quickly flared and friction was lost across the board in most asset classes. If you weren’t hedged, long the dollar or in cash, a paper cut quickly became an open lesion. Although par for the course these days, confusion swirled after parsing the Fed’s statement and what Bernanke had implied towards monetary policy in the future. Weighing the market’s response and even Bernanke himself conveying he wasn’t worried about the rise in rates to-date, the pivot in expectations the markets had initially made in May towards a tapering of monetary stimulus – held its course.

Whether you agree or disagree with the Fed’s push towards transparency and candid whispers to the markets, the transmission exchange that once was dropped from seemingly a black helicopter by the likes of Greenspan and Volcker, is now stick shifted from the podium and the press corps with a considerable lag towards material actions by the Fed. Whose to say which method works best without the shadow of history to measure, but in our opinion, Bernanke does have the more delicate task of working with the disinflationary and deflationary side of the continuum than the mighty Volcker who beat inflation with his big blue ox and long handled axe…

We kid, although taking nothing away from the stalwart performance of the former Chairman, with considerable historic record towards the interest rate cycle, tops are violent and exhaustive – while cycle lows are long and drawn out affairs. In many respects it is the mirror of how the equity markets trade, whereas, tops are often a process – while lows are a much clearer structural signal to define. In our opinion, we continue to find journalists, pundits and market participants not adjust their perspectives on inflation, rates and monetary stimulus to the backside and southern hemisphere of the cycle where the drains run counter-clockwise and punctuality is a relative expression.

Considering the global connectivity of markets and economies these days, and that it’s been roughly 70 years since the Fed had to navigate a trough – take the academics and pundits criticisms and suggestions with a grain of salt and a decanter of tequila. And let’s not kid ourselves, we’re all tourists on this vacation – some more than others.

Not-so-random thoughts

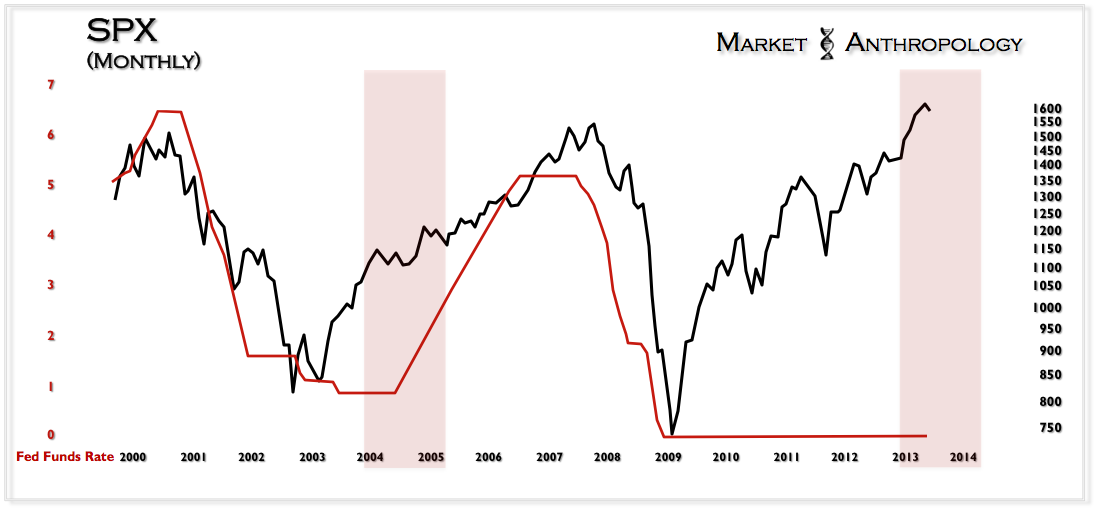

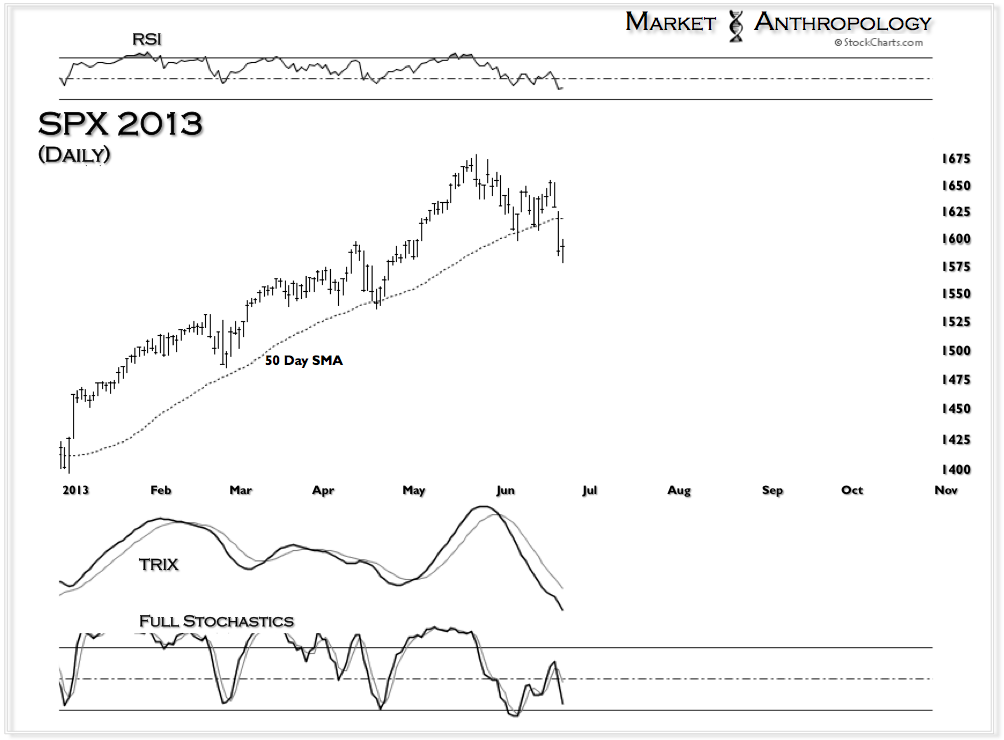

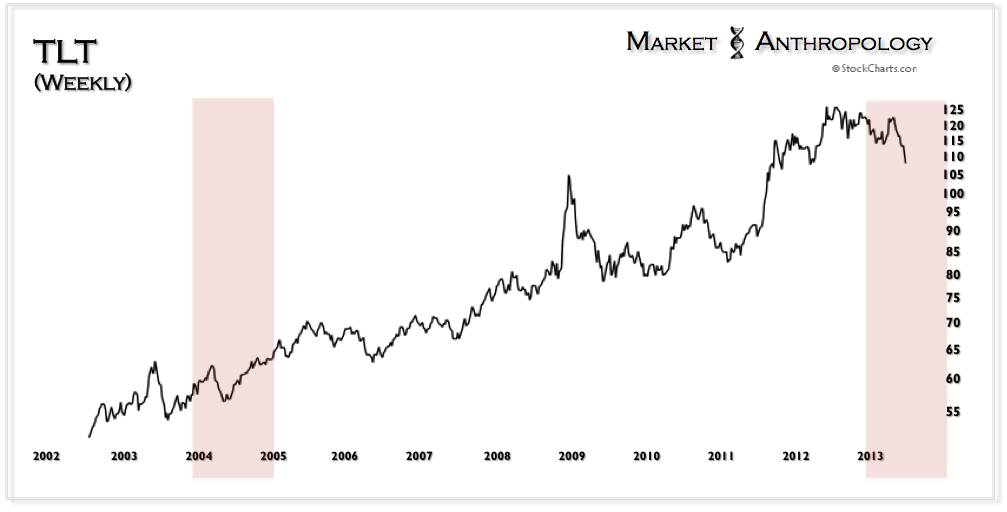

Not surprisingly, the equity markets continue to have indigestion with the ramifications of a shift in posture that is now moving towards the tightening cycle of accommodative monetary policies. Although we have explored in recent weeks the 1994 scenario where the Fed surprised the bond and equity markets with a rate hike and expectations of further tightening, we thought we would also consider the withdrawal of QE a comparative measure to the Fed’s pivot and first rate hikes in 2004.

In light of the equity market’s long-term Meridian break this spring and the shift in posture by the Fed, we resurrected a few proportional stimulus concepts initially floated by us back in the first half of 2011 that argued although near term volatility and retracements were likely, longer-term, the equity markets had room to run once accommodative monetary policies were withdrawn.

Dow 20,000?

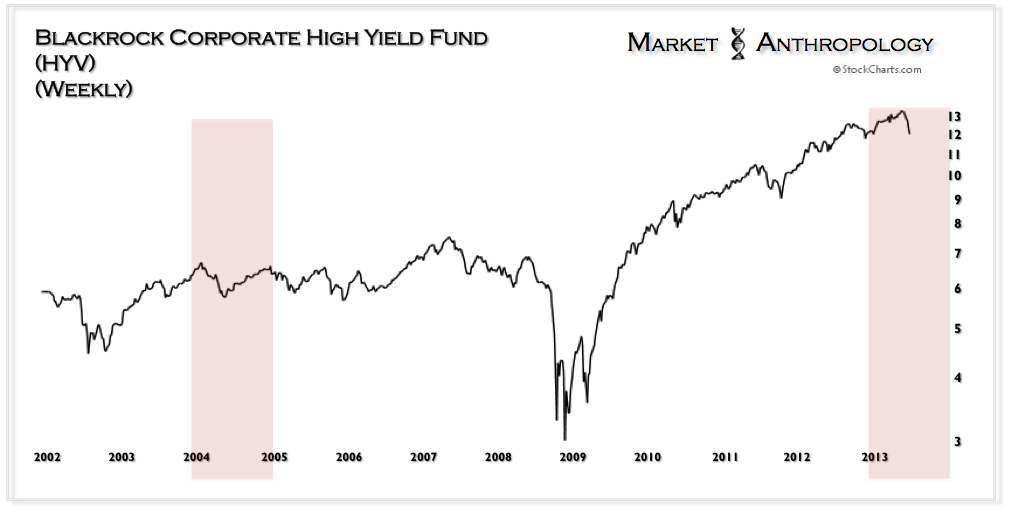

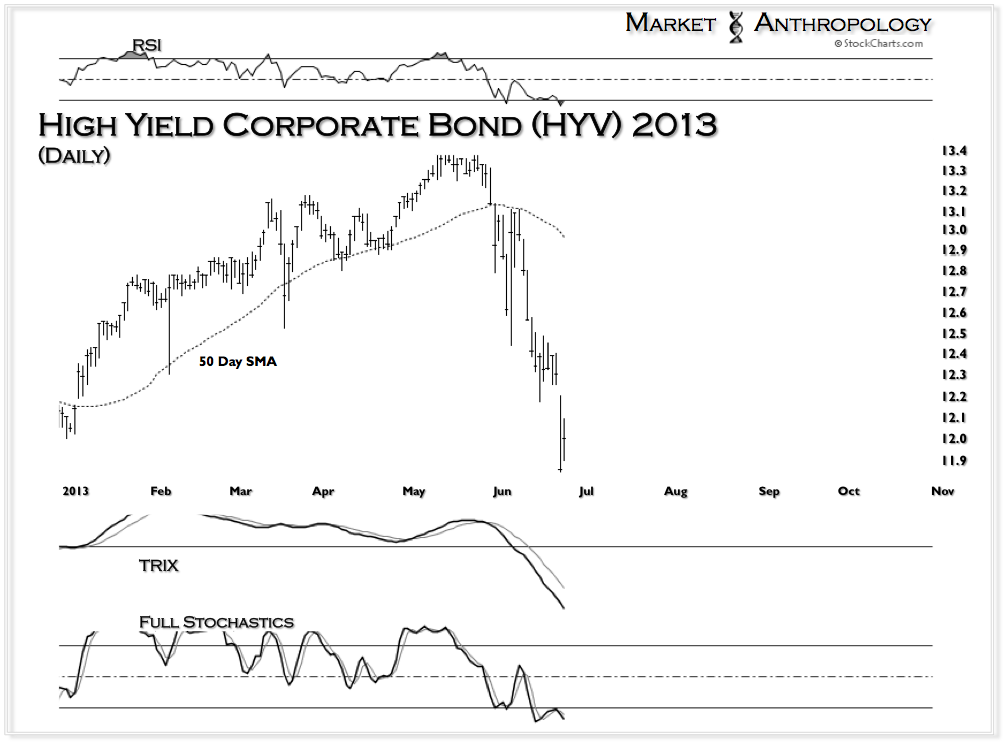

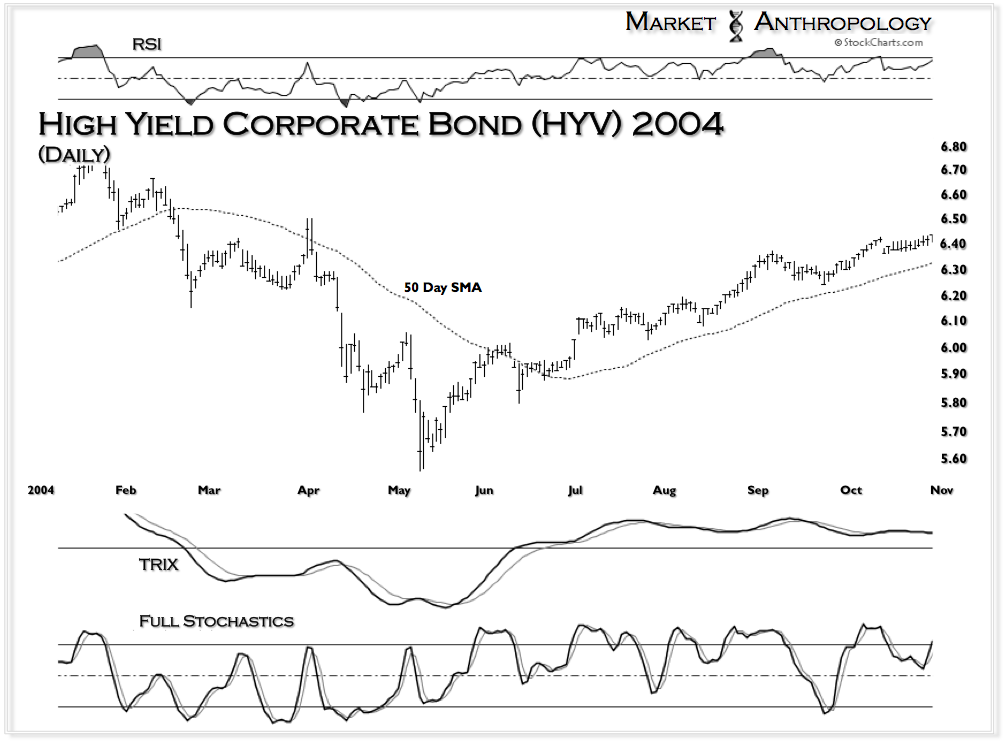

Almost two years later, the stimulus “injections” have continued to the greatest benefit of the equity markets and assets that favor historically low rates – such as high-yield bonds. The last time we had commented on the high yield sector was way back in March of 2011 as the markets were driving towards the finish line of QE2 – and when we still wrote from a singular first person perspective…

“When I think about the Big Picture and forming guesstimates of the future – I like to look at the proportions of the contributing forces. The chart below provides an excellent example contrasting the two most recent recessions and reflations and their effects to the low-grade corporate credit markets.

…Sure I’m taking the liberty of extrapolating past performance to shape my future expectations. But what has really changed here – except for weakening the accounting standards and increasing the velocity of stimulus by the Fed? The Fed has really just moved the Credit Bubble from real estate speculation over to the corporate ledger side of business.

Is that a healthier bubble? Probably. Will that put a strong bid under the market going forward over the next few years? Probably. But they are still altering the time continuum and who’s to say if they got the memo to wear the bullet proof vests when the Libyans come calling…“Dow 20,000?

Once again nothing has really changed expect the proportions have expanded even further, and perhaps this time around (and as was the case in 2004) – assets such as Blackrock’s high-yield fund have reached their high water mark for a spell.

If that is in fact the case – and assuming China, Europe or some other exogenous crisis doesn’t upset business and consumer sentiment domestically, the next stage for the US economy is for those corporations flush with easy money over the past five years to put that capital to work in the economy.

The Congruent Market

Despite what some may believe, the decrease in monetary accomodations has historically been met by the equity markets as near term bearish but longer term bullish. This was the case in 1994 – as well as in 2004.

Back in April of 2011 we had noted the similar reflationary waves instigated and nurtured by the Fed as The Congruent Market Theory. Granted, at that time we had compared the monetary and equity environments to 2004 due to our expectations that the Fed would let the economy stand on its own two feet after QE2 concluded. Of course, QE2 wound down in the first half of 2011 and the equity markets quickly chocked on indigestion from the confluence of a US debt downgrade and another firestorm in Europe.

Will it be different this time around is up to the rocket scientists at the Fed to determine if the economy has critical mass to escape some of the latent gravity of the previous crisis. Bernanke appears to imply it will.

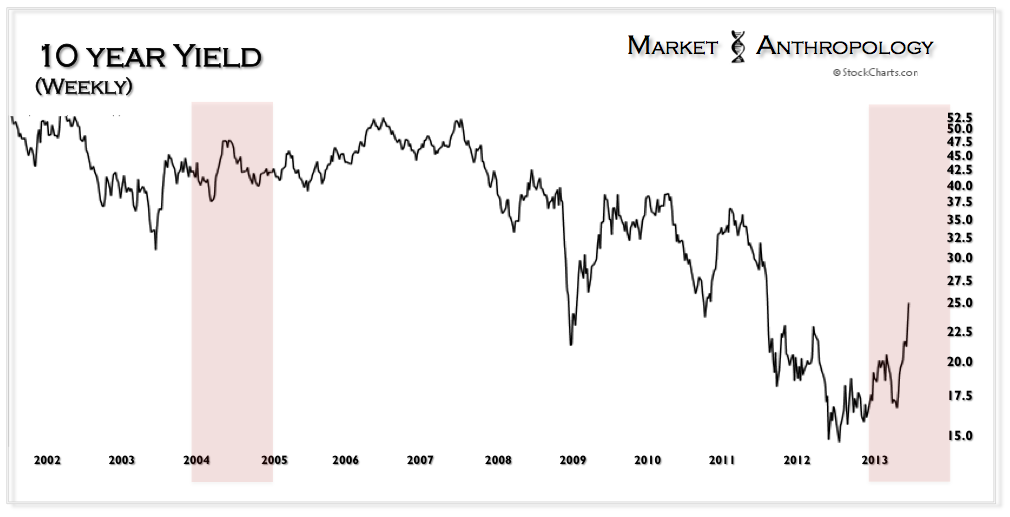

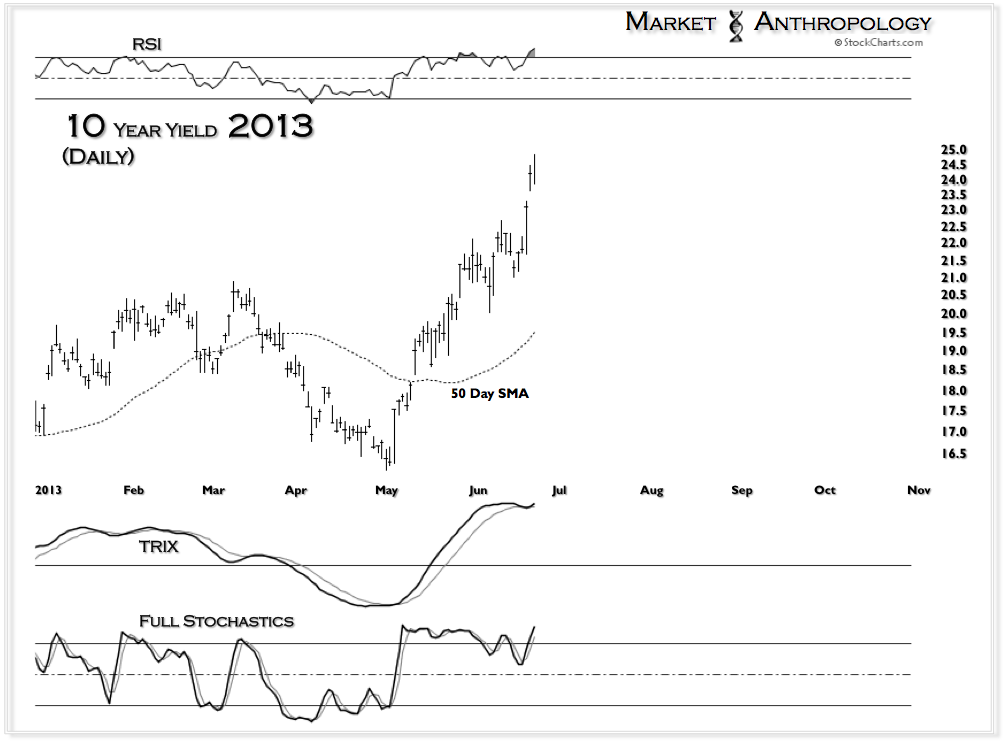

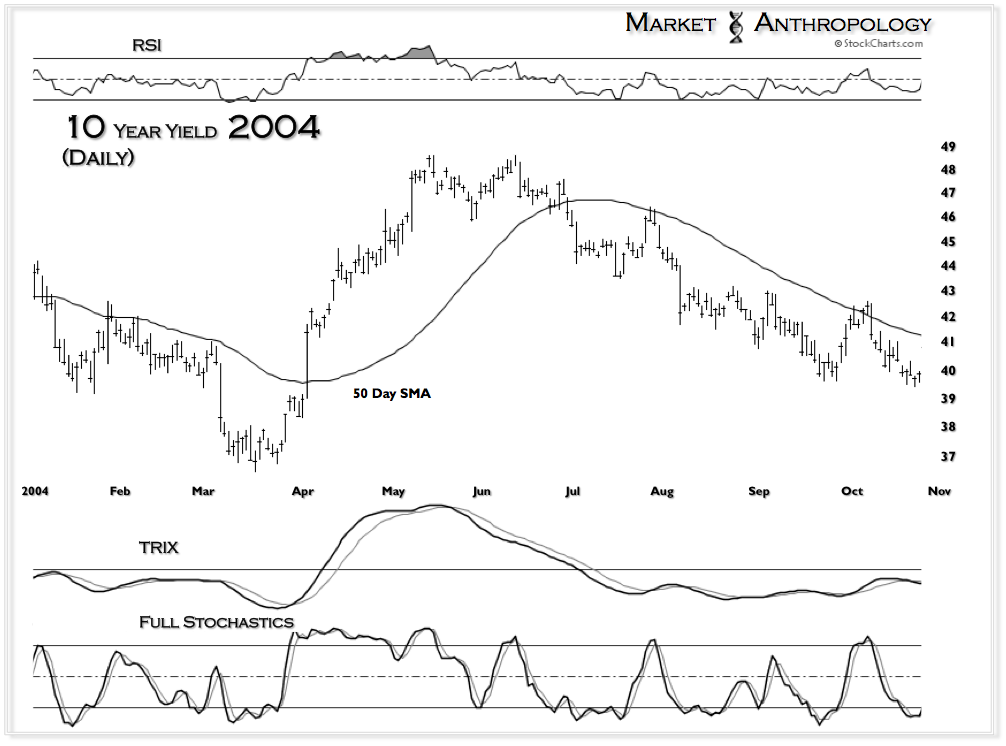

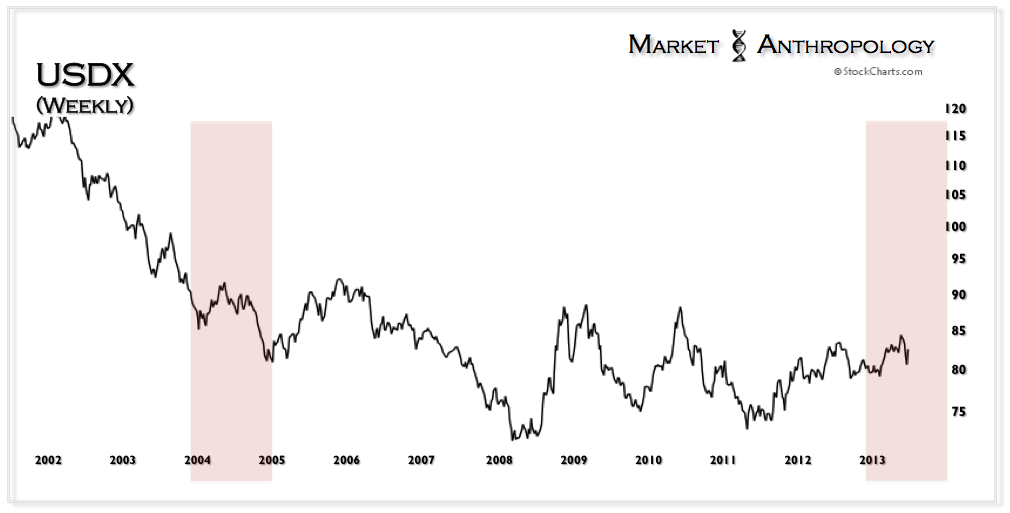

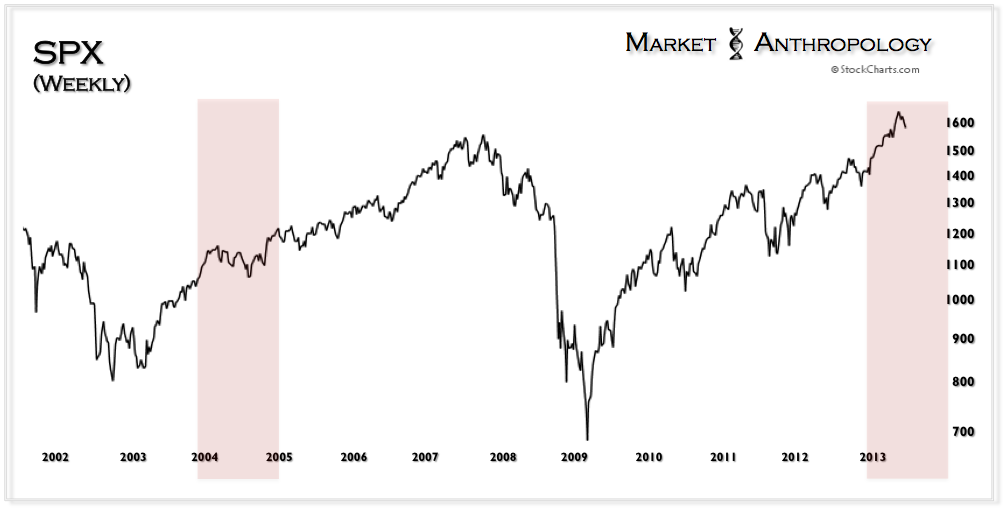

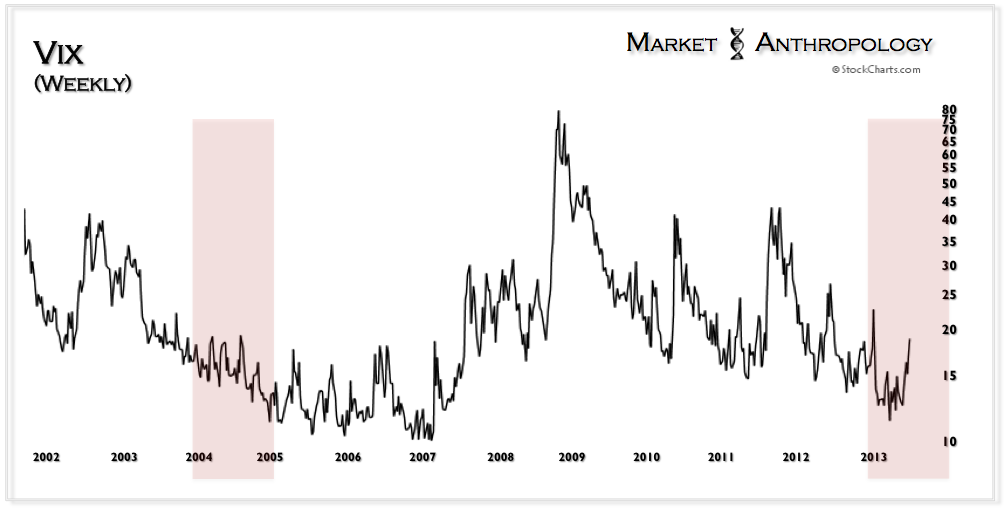

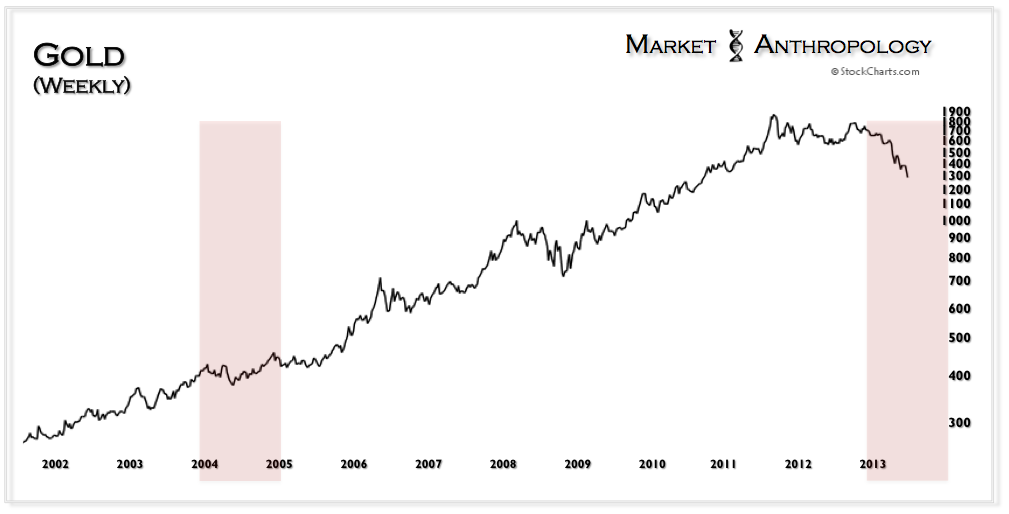

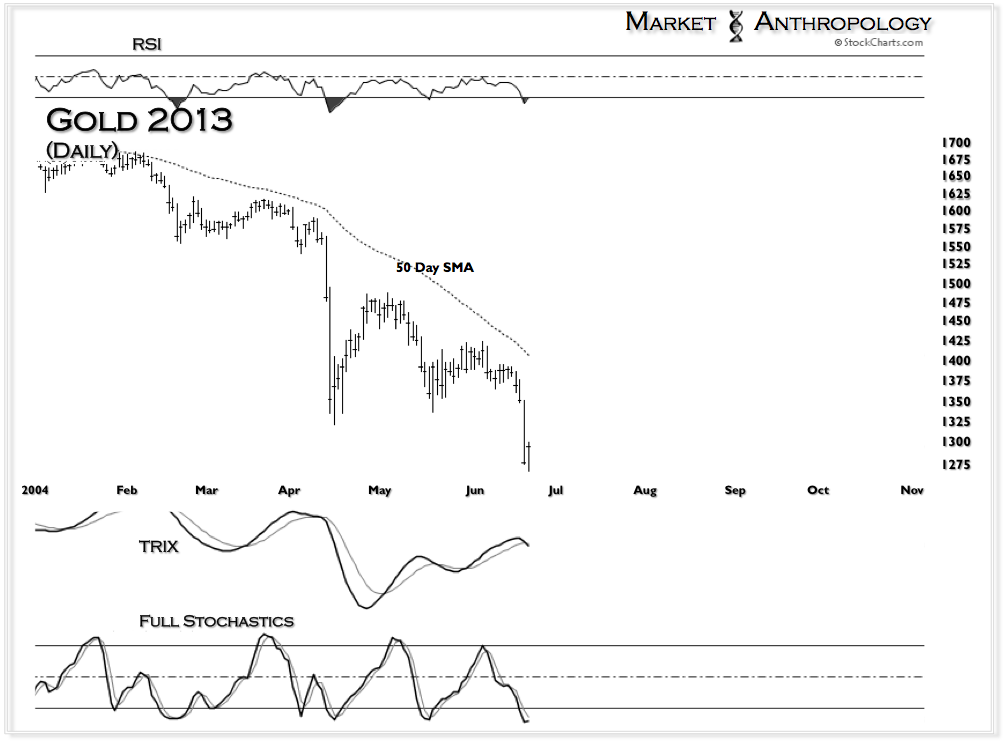

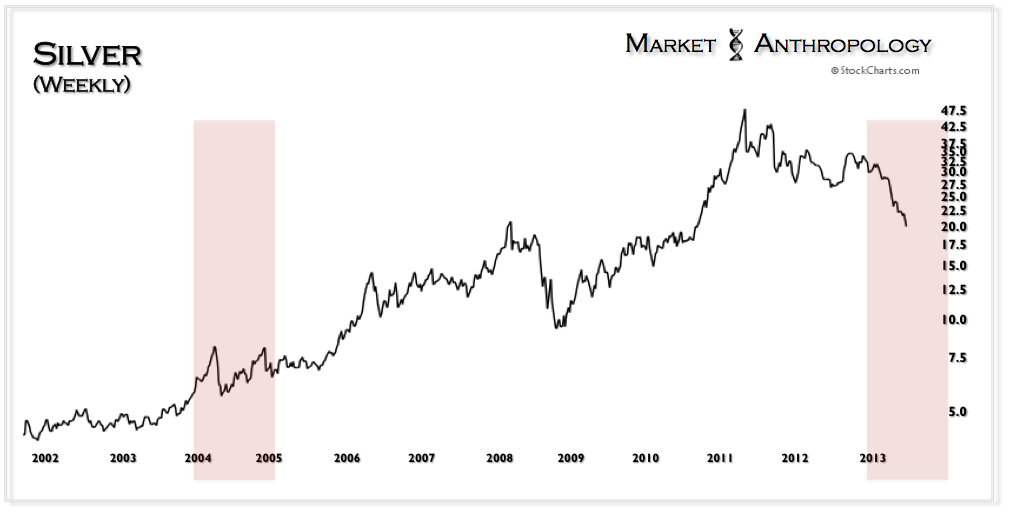

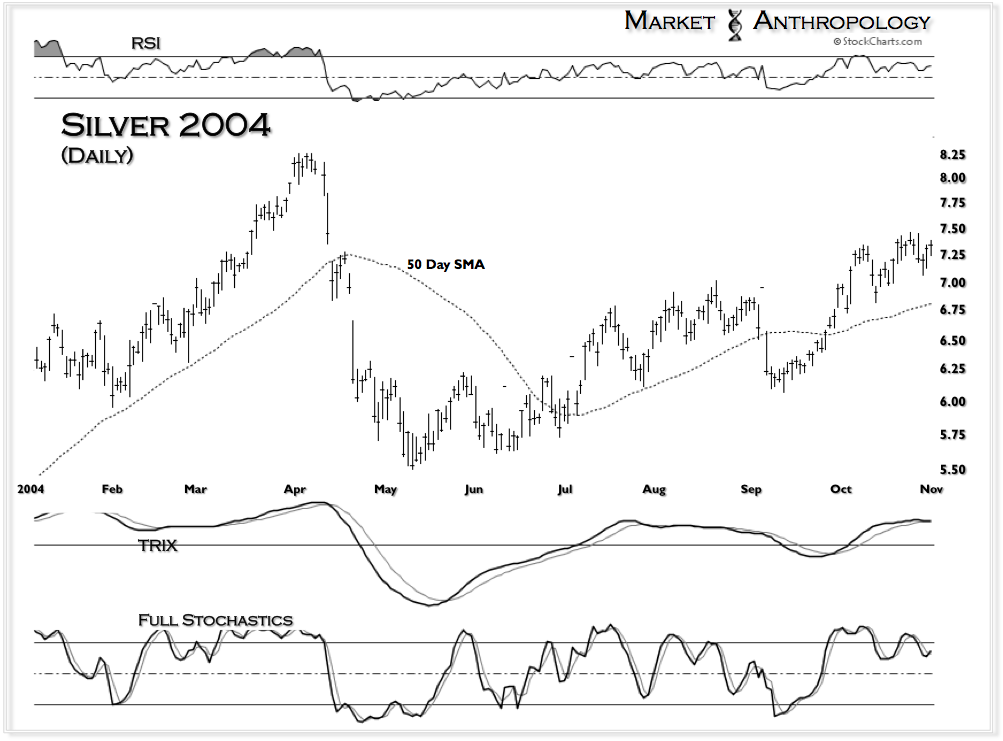

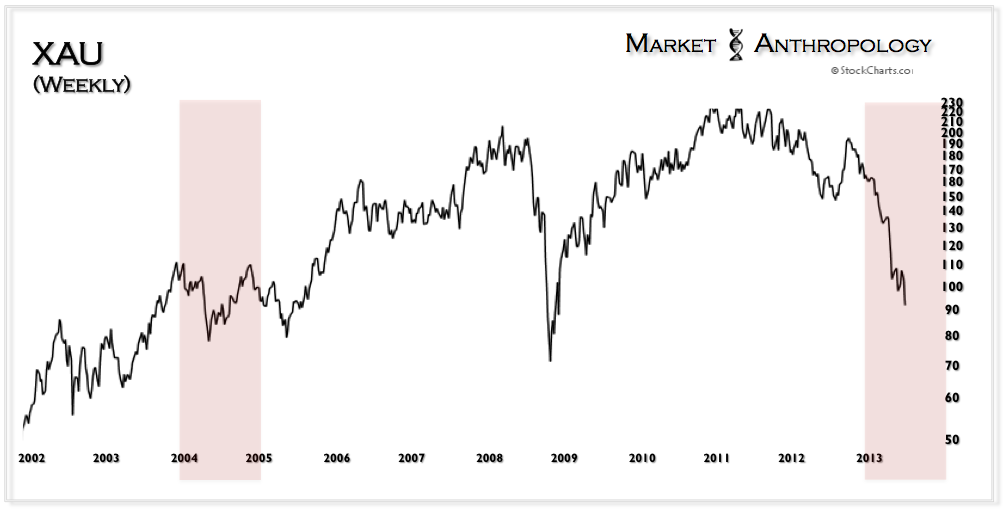

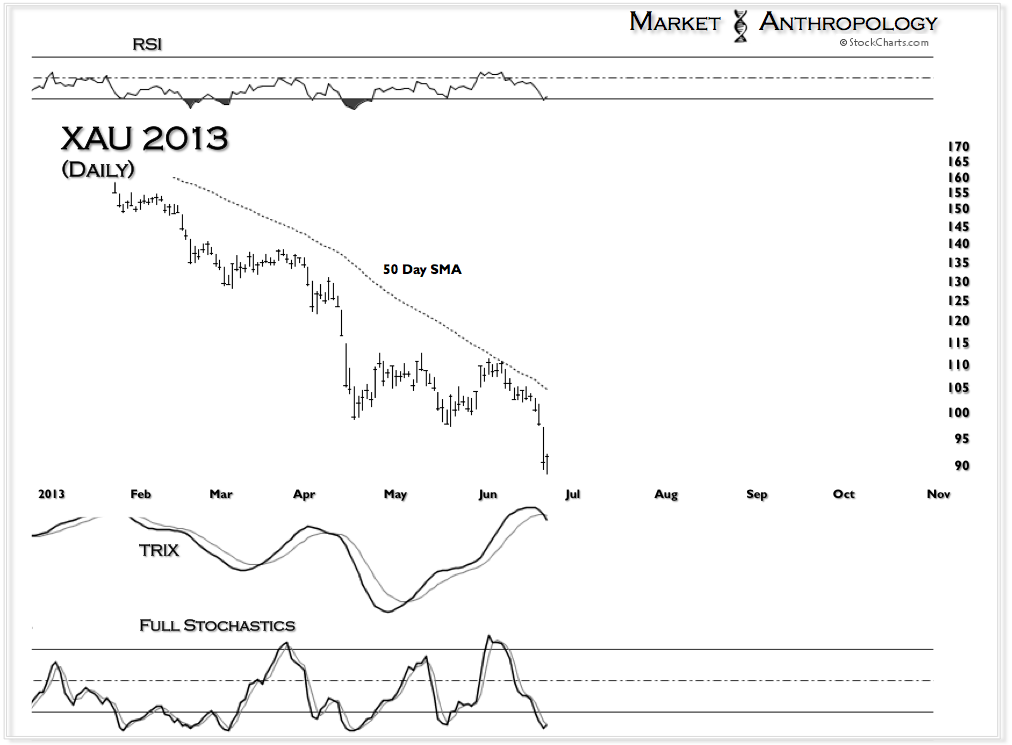

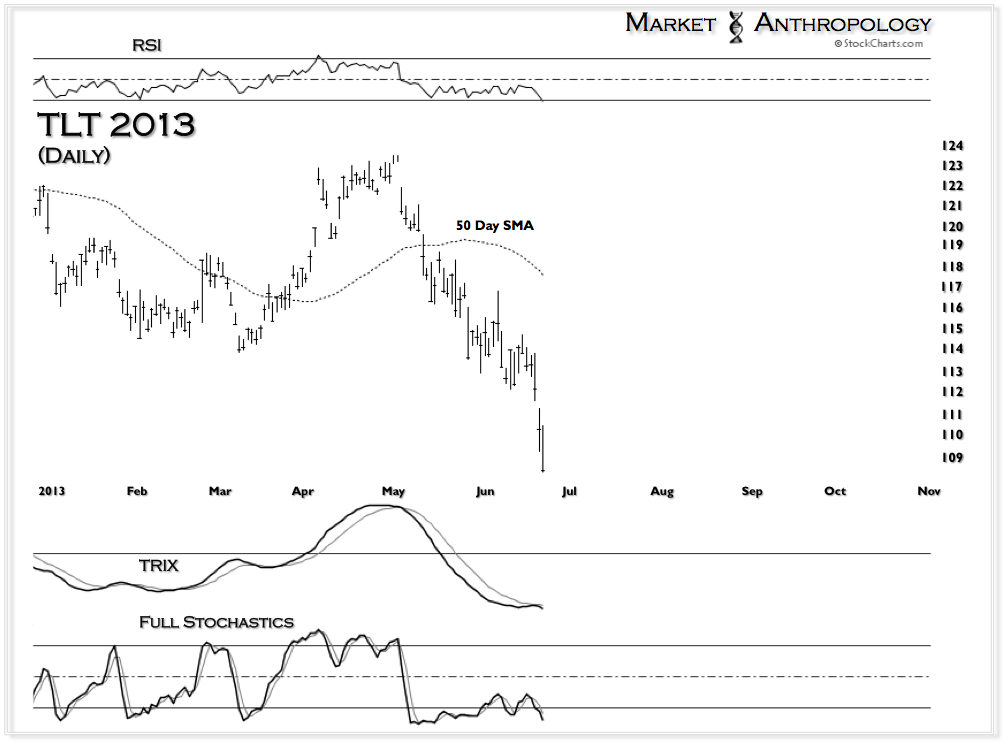

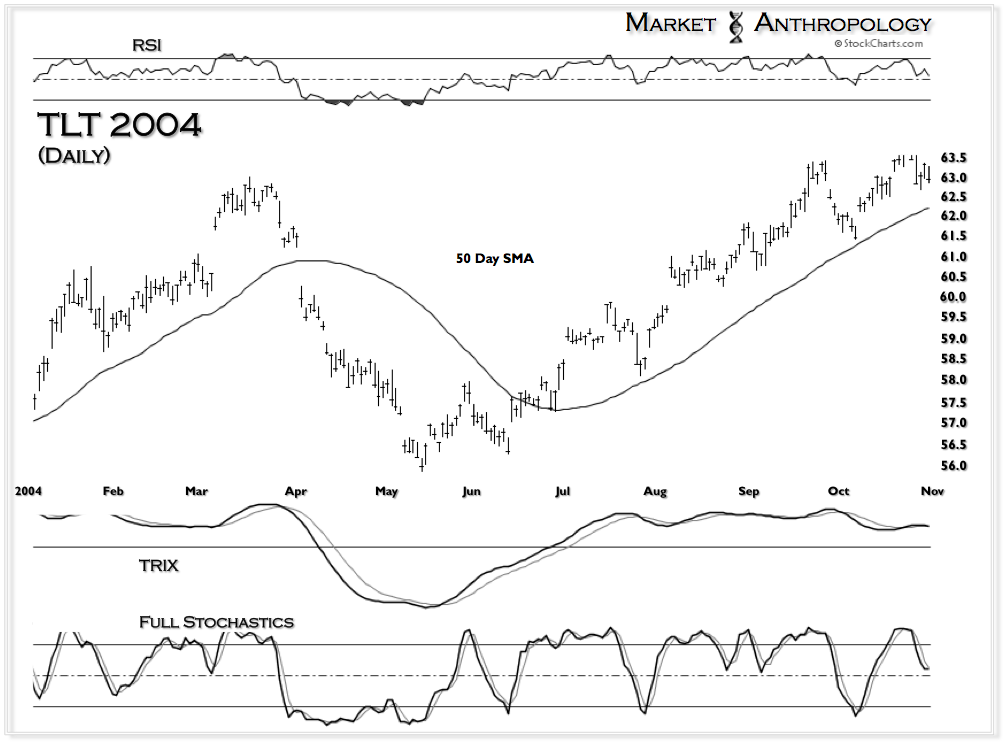

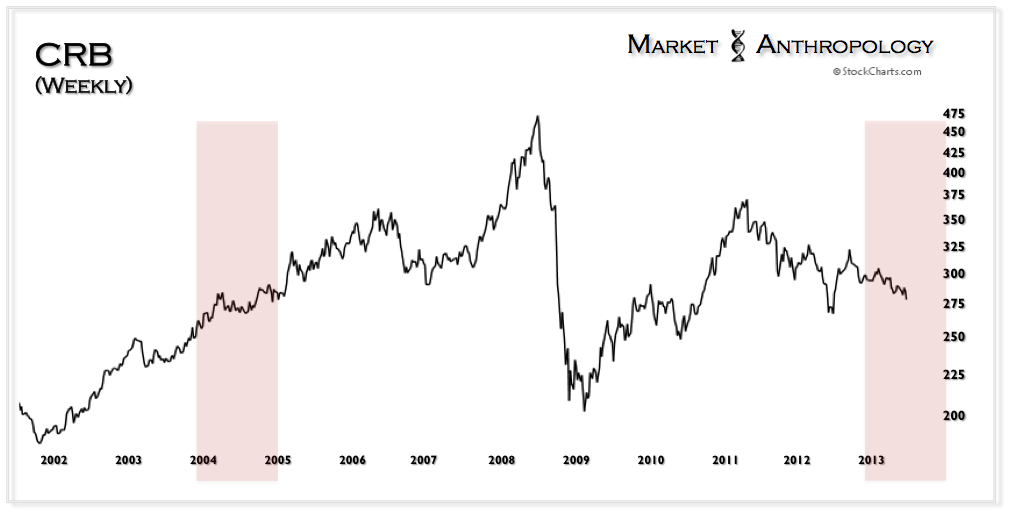

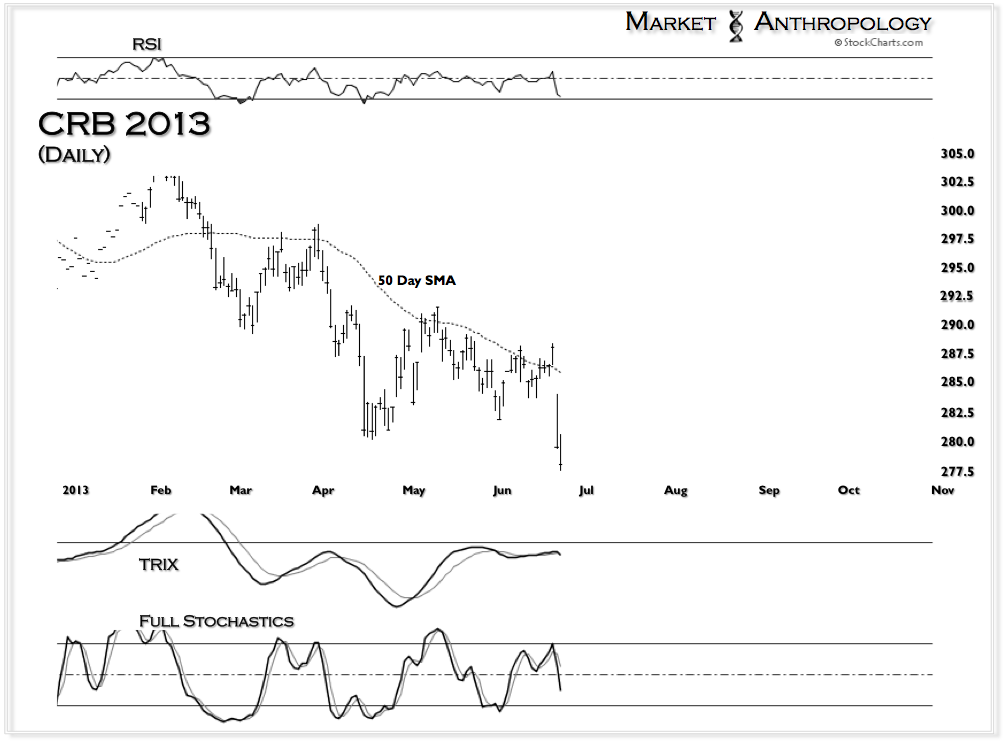

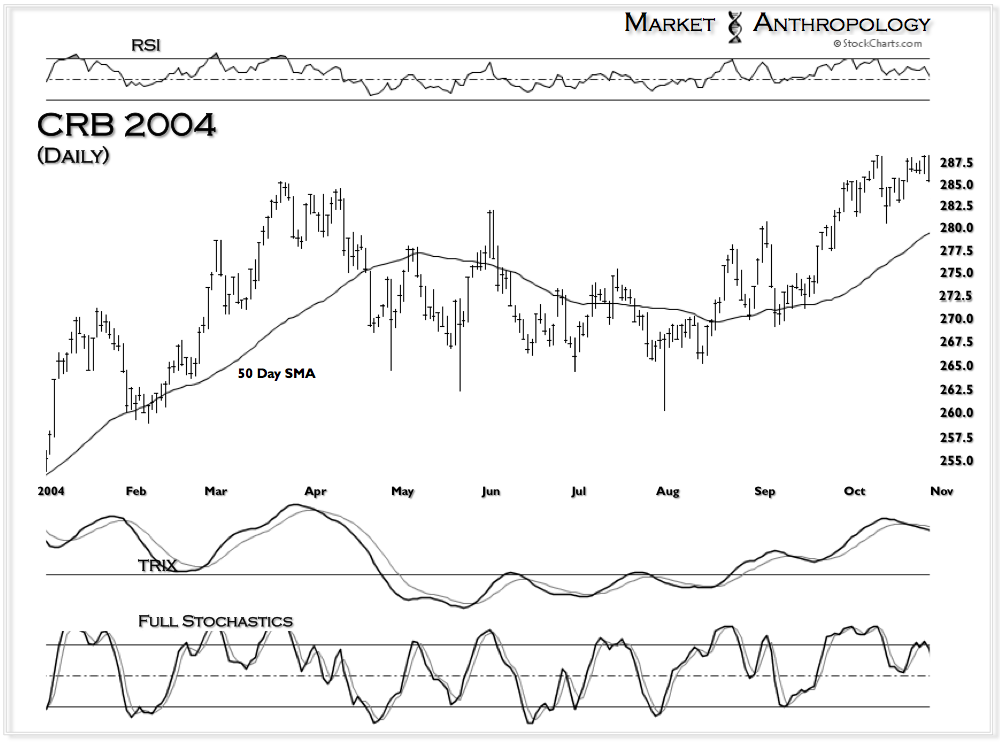

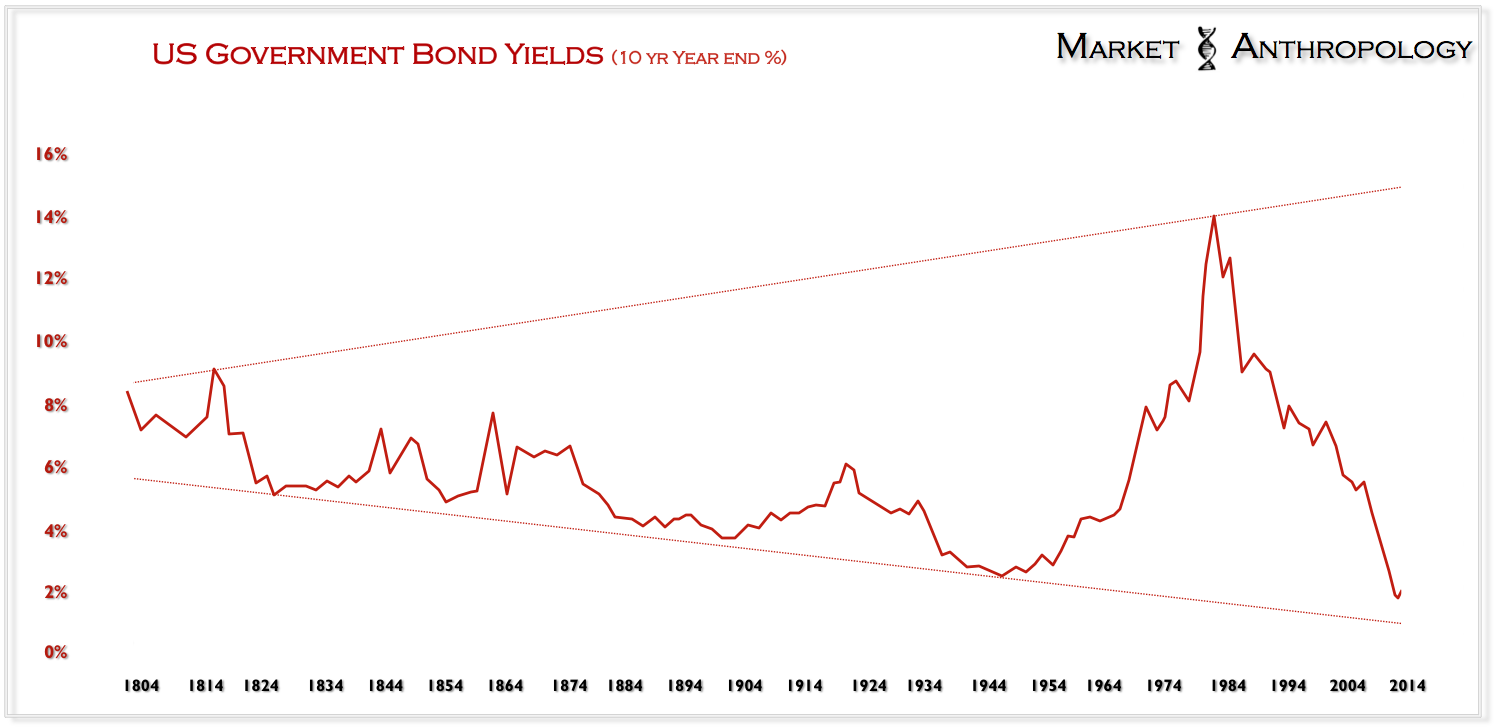

A Closer Look – 2004/2013

Below are 11 markets and metrics that show the congruences and contrasts between 2004 and today.

Click to enlarge images

{kind=link}