Despite any obvious correlations, there is always information to be gleaned in comparative cycle work. What’s past is prologue; a benchmark – and what’s present can be contrasted with the past for bearings and innuendo within the current market environment. If your timeframes run longer than a life cycle of a mosquito, but less than a 17 year cicada – ignoring the nuances of market history will likely result in the markets swatting such ignorance – as well as your wealth. Just as a historian places certain current events within a broader historical narrative for context, the same should be applied to the markets with respect to the basics of duration, performance and character. In a behavioral system that neither “creates or destroys” market psychologies – we have yet to find a simpler tool at remaining somewhat rational and grounded within the perception of at times an irrational construct. It is all uniquely – the same.

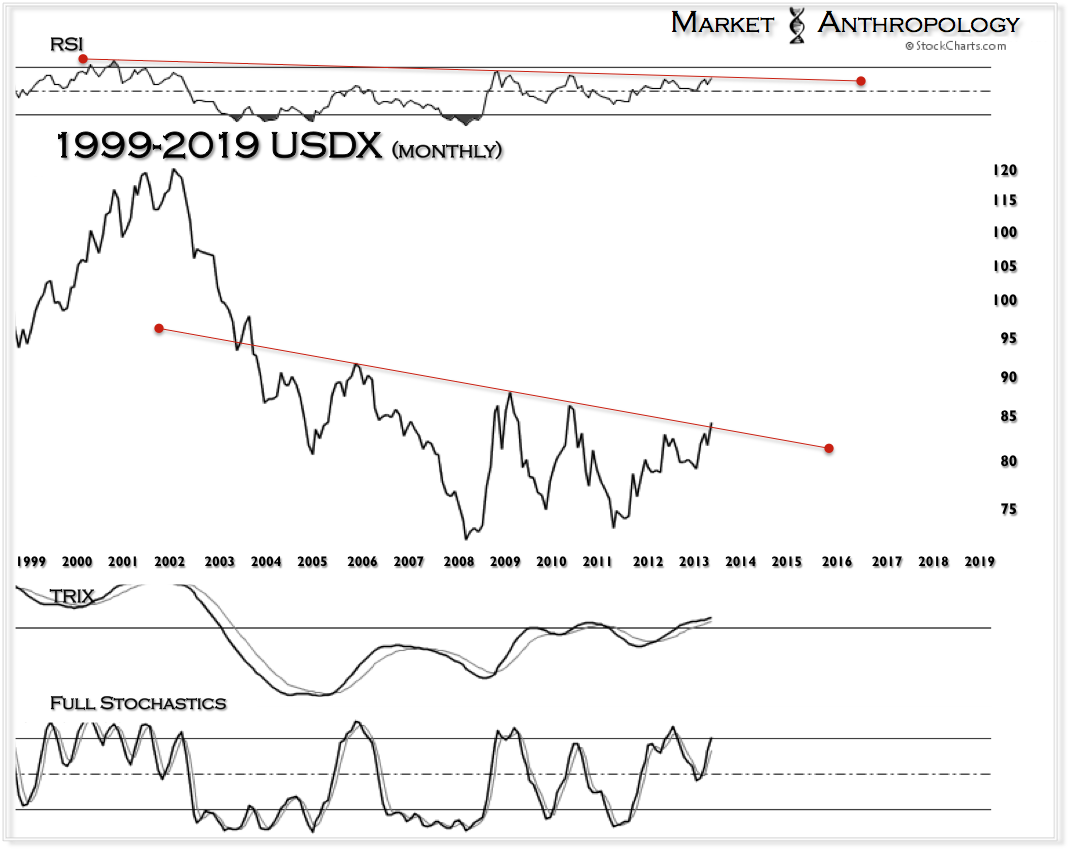

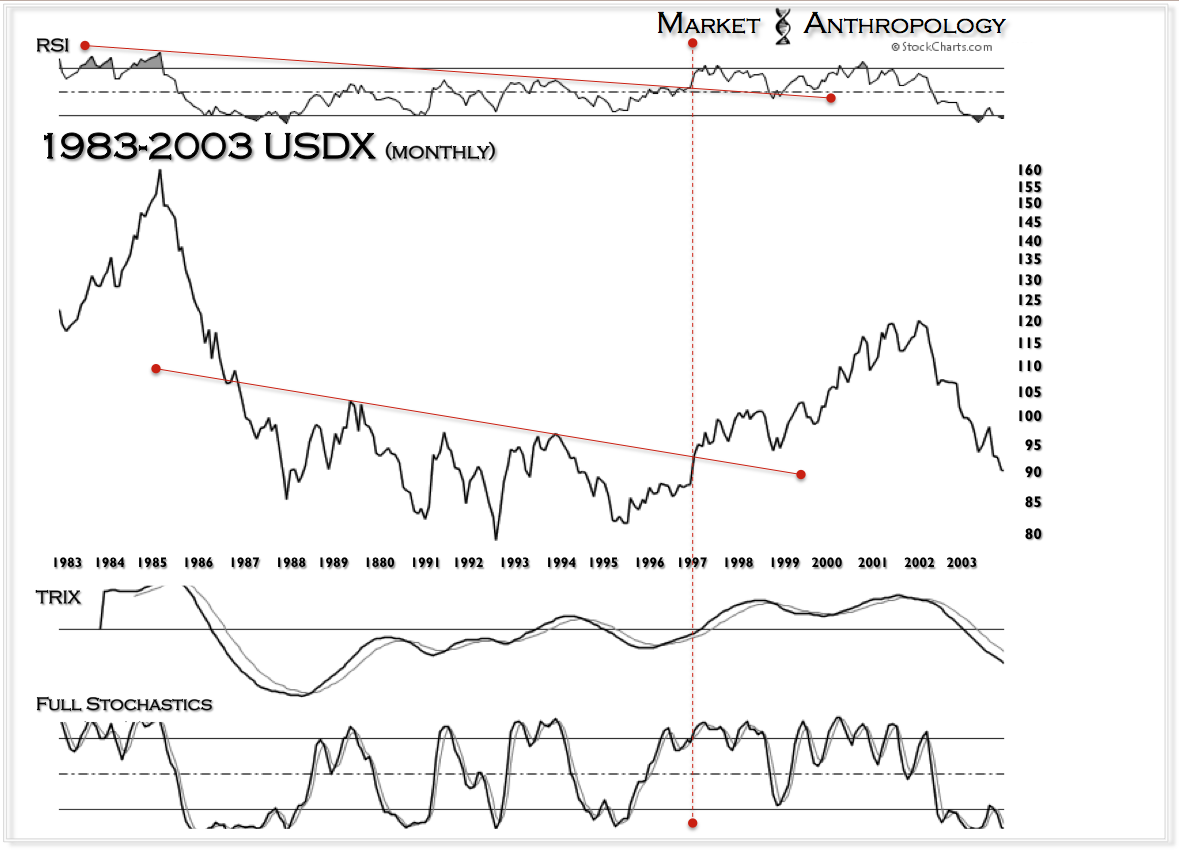

With that said, here are a few updates of our Secular Tides concept we have commented on in a variety of iterations over the past two years. Although we have typically posted the RUT:SPX ratio in our weekly updates, for clarity purposes – we utilized the inverse (SPX:RUT) as it runs with the US dollar index. Like the previous turn in the 1990’s, the dollar has led the pivot higher as the primary “tide” – with large cap stocks getting pulled higher relative to the RUT as the secondary tide.

The most notable divergence today when contrasted with the dollar’s last breakout leg during the first half of 1997 – was the considerable strength of the move as shown in its RSI. While the dollar’s current momentum profile mimicked the previous cycle’s range through April – it has recently diverged over the past month.

With only a few sessions remaining in May – the US dollar index is marginally holding above it monthly breakout ~ 83.50. As we see it, the risk here for dollar bulls and precious metals bears (both of which we have helped chair the Departments since April of 2011) – is the dollar becomes exhausted and similar to 1994 takes another trip lower through the range. All things considered – we still like the dollar, but remain vigilant and open to an audible lower for a spell.

|

|

|

Click to enlarge image

____________________

* Subsequent overlays and renderings completed by Market Anthropology

|