Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

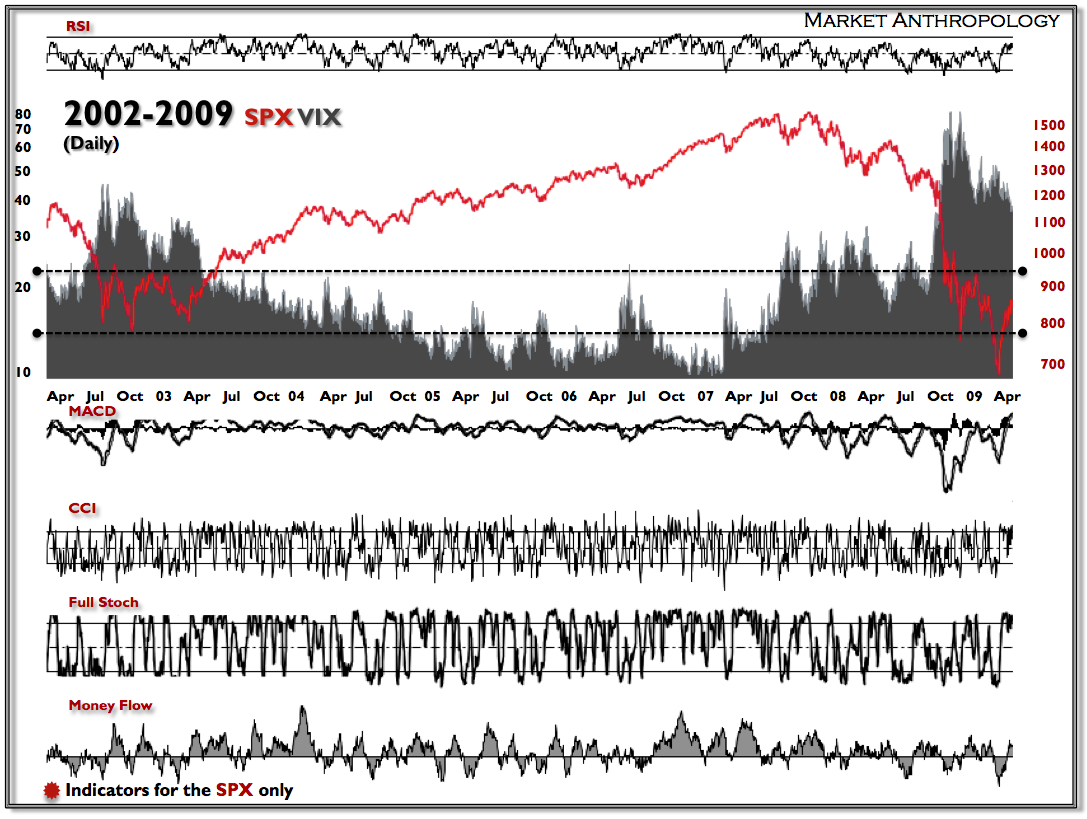

In December of 2008 as the market was reflexively trading higher out of the November lows, there was a great deal of chatter by traders about “the” low being made for the cycle. And while the selling pressure was tremendous in both October and November (momentum low), and the market was up by more than 20% from the lows by the end of the year, I wanted to look for another perspective to see if there was any evidence to the contrary. I found it in the VIX while reviewing similar market environments in 2002 and 1990.

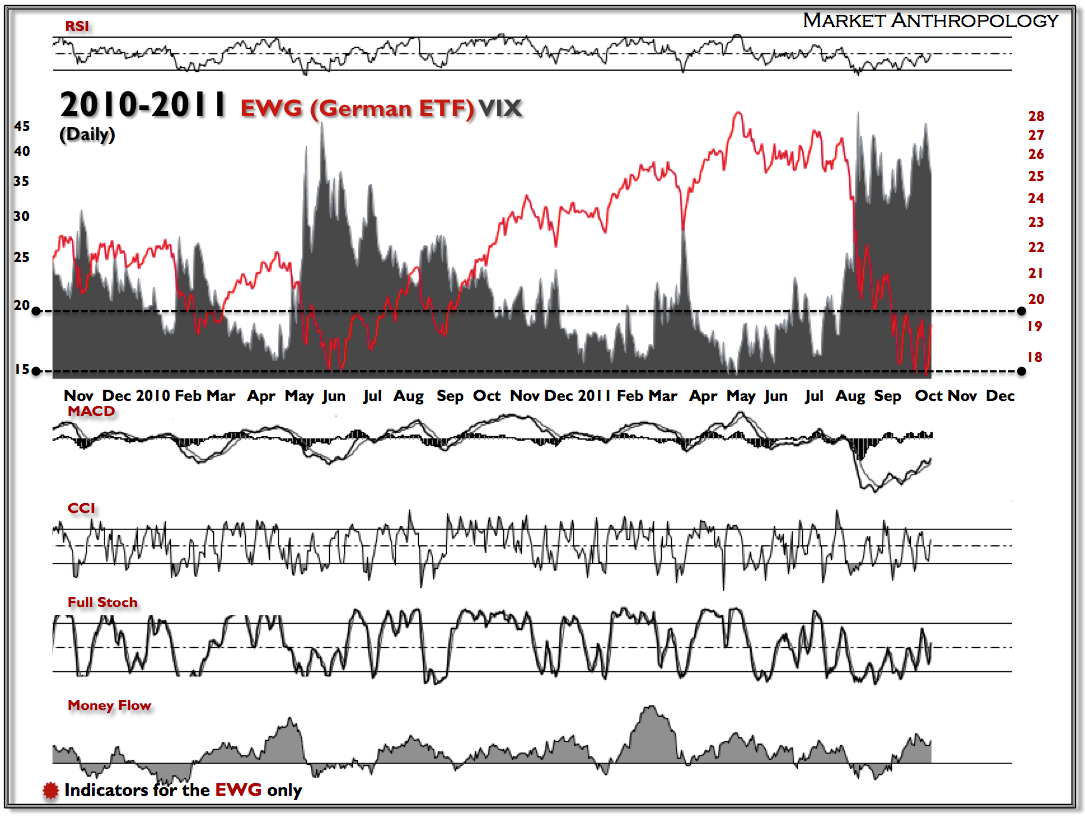

As you can see below in the charts, both bear markets found their exhaustion points at lower highs in the VIX. Considering the market back in December of 2008 was trading out of a higher VIX print in November, it constructively colored my expectations for the beginning of that year.