Where Reflexivity Meets Equilibrium

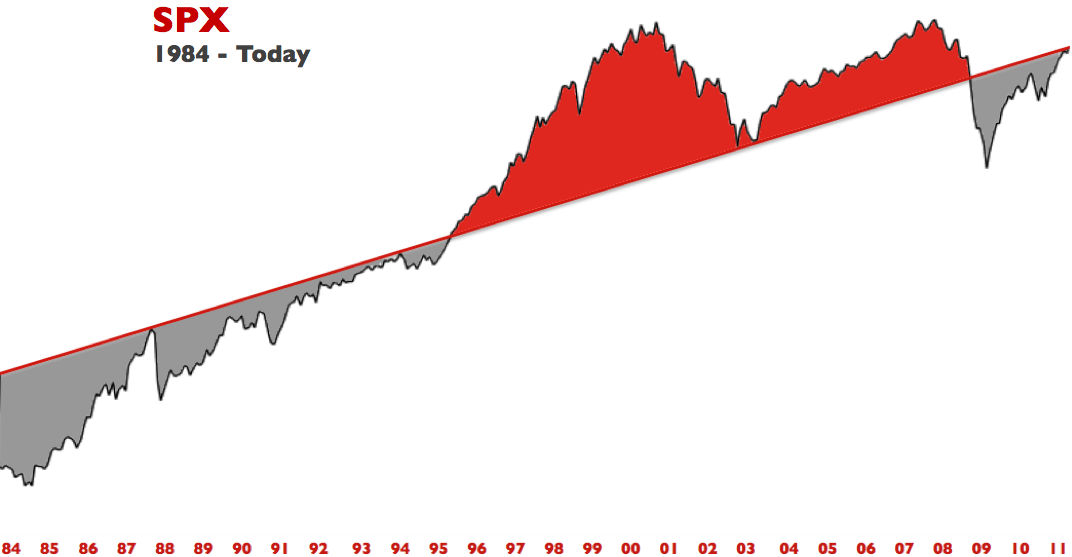

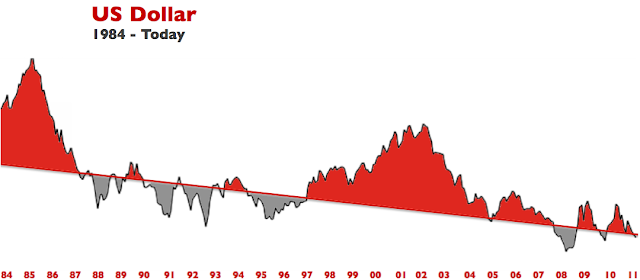

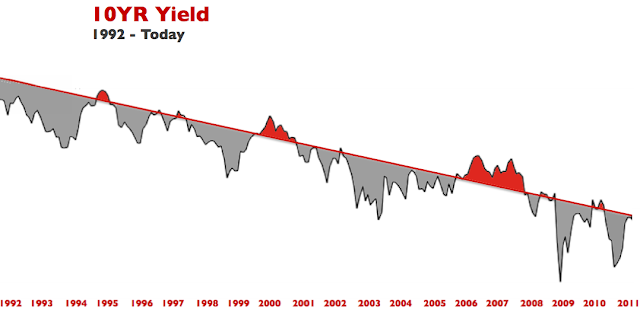

Here are a few charts of different asset classes with my Meridian Theory applied through their respective trends. Each chart utilized the same reference dates as crosses to establish the meridians.

In essence, the shading represents time periods where the markets are at a disequilibrium with the trend. In my unified theory (tongue in cheek once more), the meridian represents an equilibrium, which could be construed as the overlap between Soros’s theory of reflexivity and traditional equilibrium thought. This makes rational sense, since it has typically represented where the market has either found equilibrium – or lost it altogether. In 1987, it represented the top of the trading range out of the historically depressed markets of the 1970’s. The gains were steep, the programs misfired, mass psychology took over and the rest is history. After the 87′ crash, the market eventually made its way back to equilibrium and crossed the threshold right before Greenspan invoked the self fulfilling prophecy that was Irrational Exuberance. In 2002 and 2003, the market found its balance at the meridian and started its reflationary ascent to the 2007 highs. In 2008, it represented the threshold where the markets lost their footings – due to the financial crisis, and crashed. Today, with the exception of the commodity and gold sectors, these markets have worked their way back to equilibrium – as represented on the charts. Click to enlarge the charts.

Assuming all things are relative, and the kinetic intra-market/asset class relationships still apply – you can see why George Soros believes that the gold market is the largest asset bubble of the day, and by extension the commodity complex as well.

These charts illustrate that thought rather profoundly. It would be an excellent time for him to put his money where his theory applies and dwarf the gains he reaped for breaking the British Pound. Ironically, the catalyst this time may be realized when the financial system and the global economy are found to be in better shape than most suspect, and that once the stimulus is slowly removed… surprise, surprise – life goes on and the markets function.

With that said, a dislocation of this magnitude would likely have negative impacts to the equity markets in the short to intermediate time frames. So stay frosty. More to come in this line of thinking.